The Revenge Trade: Anatomy of the Most Destructive Pattern in Active Trading

The revenge trade does not feel like revenge when you take it.

Every active trader takes revenge trades. The frequency varies by experience level and by the structural constraints the trader has or has not built around their process, but the impulse itself is universal. It emerges from a specific convergence of psychological factors that are nearly impossible to suppress through willpower alone: loss aversion, the need to restore a mental account balance, urgency amplified by recent pain, and the cognitive distortion that a trade taken immediately after a loss has a better chance of recovering that loss than any other trade.

None of those factors are accurate representations of reality. The market does not know or care about the previous trade. The probability that any specific setup works is not altered by the outcome of the trade that preceded it. The urgency to recover is a product of emotional pain, not of genuine opportunity. The trade that feels most compelling in the minutes after a stop-out is almost never the trade that the written strategy would identify as the highest-quality available setup. It is the trade that is most visible, most emotionally salient, and most proximate to the pain that demands resolution.

This newsletter is about why the revenge trade happens with such reliability, what it actually costs across a trading career, the specific mechanisms that generate it, and what structural interventions prevent it from occurring rather than simply requiring willpower to resist in the moment.

[Download the full printable PDF below.]

WHAT THE REVENGE TRADE ACTUALLY IS

The term is commonly used to describe any trade taken in anger after a loss, but that definition is too narrow to be useful. The revenge trade is better defined as any trade taken primarily in response to the emotional state created by a preceding loss rather than in response to a genuine setup meeting the strategy’s criteria. This definition captures a broader and more accurate picture of how the pattern actually manifests.

Under this definition, the revenge trade does not require the trader to feel angry. It requires only that the decision to enter was driven more by the desire to recover the preceding loss than by the quality of the available setup. A trader who takes a valid-looking setup thirty seconds after a stop-out, without conducting the same pre-entry evaluation they would have conducted had no loss occurred, is taking a revenge trade even if they feel calm and professional at the moment of entry. The problem is not the emotional intensity. The problem is the contamination of the decision process by an outcome that is irrelevant to the quality of the next trade.

There are several recognizable variants. The immediate re-entry is the most obvious: the trader stops out, immediately re-enters the same instrument in the same direction, citing the same setup logic with none of the reflection that a genuine re-evaluation would require. The escalated re-entry is more dangerous: the trader stops out, re-enters the same trade at larger size to recover the loss faster, transforming a controlled one-percent loss into a potential two or three percent loss on the follow-up. The displaced revenge trade is the subtlest: the trader stops out on one instrument, then takes an oversized or under-evaluated trade on a completely different instrument, as if geographic distance from the original loss provides the psychological distance that is actually absent.

PRACTICAL APPLICATION

For the next thirty days, tag every trade in your journal with the time elapsed since the previous trade closed. Then filter your journal to show only trades taken within fifteen minutes of a stop-out and calculate the average R for that subset. Compare it to your average R for all other trades. For most traders who have never run this analysis, the gap is immediate and stark. The fifteen-minute window after a stop-out is one of the lowest-quality execution environments in a trading session, and the data almost always reflects this before any behavioral change is attempted.

THE PSYCHOLOGY BEHIND IT: WHY THE BRAIN DEMANDS RESOLUTION

The psychological mechanisms that generate the revenge trade are well-documented and operate below the level of conscious reasoning. The most fundamental is loss aversion — the empirically established finding that the psychological pain of a loss is approximately twice as intense as the psychological pleasure of an equivalent gain. A one-percent loss is not experienced as the mirror image of a one-percent gain. It is experienced as a significantly more negative event, which means the emotional pressure to undo it is disproportionate to its actual financial significance.

The mental accounting framework compounds this. Traders, like all humans, do not experience their P&L as a continuous financial number. They experience it in discrete mental accounts — the session account, the week account, the month account — and losses within those accounts create a specific psychological discomfort that is distinct from the general awareness of being down money. A trader who is down one percent on the day has not just lost one percent of capital. They have created an open negative account in their mental ledger that generates ongoing discomfort until it is closed. The fastest way to close it is to recover the loss, and the fastest way to recover is to trade again immediately.

The availability heuristic adds another layer. Immediately after a loss, the most available trade — the one that is most salient in working memory because it is literally the same chart the trader was just looking at — receives a cognitive premium that has nothing to do with its objective quality. The brain treats familiarity and proximity as signals of opportunity, which means the worst possible trade from a strategic standpoint, the immediate re-entry on the instrument that just stopped out, is simultaneously the most cognitively available and the most emotionally compelling option.

“The trade that feels most necessary to take immediately after a loss is almost never the trade that the strategy would identify as most worth taking. Urgency and opportunity are different things.”

PRACTICAL APPLICATION

After any stop-out, conduct a brief written check before taking the next trade. It needs to answer only one question: am I evaluating this setup the same way I would evaluate it if no loss had just occurred? Write the answer honestly. If the answer is no, or if the question itself feels irritating to engage with, the setup is being evaluated through the lens of the recent loss rather than on its own merits. That is the moment to step back from the screen for a defined period — ten minutes minimum — before returning to evaluate any setup.

THE REAL COST: WHAT THE DATA SHOWS

Most traders who believe they occasionally take revenge trades significantly underestimate the frequency and the cost. The underestimation is itself a product of the same cognitive biases that generate the behavior: revenge trades that happen to work are remembered as smart re-entries, while revenge trades that lose are remembered as the revenge trades. The selective memory systematically understates how often the pattern occurs and how much it costs when it does.

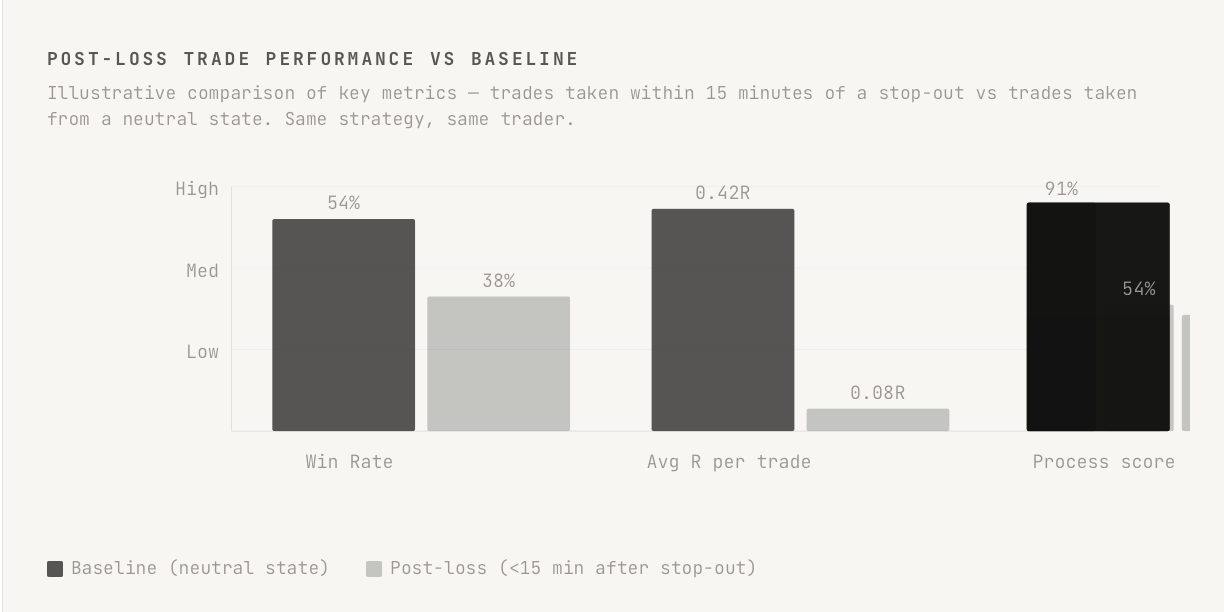

When traders track the data honestly — tagging every trade taken within a defined window after a stop-out and calculating performance separately — the numbers are consistently worse than expected. The average R on post-loss trades is lower than on trades taken from a neutral starting position. The win rate is lower. The average loss size is larger, because the emotional state that produced the entry also tends to produce wider stops, later exits, and a reluctance to accept being wrong twice in quick succession. The combination of lower win rate and larger average losses on exactly the trades that were motivated by the desire to recover is the mathematical core of why the revenge trade is so destructive.

The secondary cost is less visible but often larger over a full trading year. A revenge trade that stops out does not just produce a direct financial loss. It generates a second loss-state that is even more emotionally charged than the first, because the trader has now lost twice in a row and the second loss was specifically intended to prevent that outcome. This intensified emotional state increases the probability of a third impulsive trade, which if it also stops out creates the classic three-loss spiral that can turn a manageable one-percent drawdown into a three or four percent session loss within an hour.

PRACTICAL APPLICATION

Run a retrospective analysis on your last three months of trades. Tag any trade taken within fifteen minutes of the previous trade closing at a loss. Calculate average R, win rate, and average loss size for that subset versus the rest of your trades. Document the results and keep them visible at your trading station. The data from your own account, showing your own specific numbers, is far more persuasive than any general principle — because it converts an abstract behavioral tendency into a concrete, personal cost with a specific dollar value attached to it.

04

THE ESCALATION TRAP: WHEN SIZE BECOMES THE WEAPON

The most financially dangerous form of revenge trading is not the immediate re-entry at normal size. It is the escalated re-entry — the trade taken at increased size specifically because the larger position will recover the previous loss faster. This variant transforms a behavioral problem into a risk management catastrophe, because it combines the low-quality decision-making of the post-loss state with an exposure size that the account and the strategy were never designed to support.

The logic that drives escalation feels coherent in the moment. The trader lost one percent. A two-percent position that wins will not only recover the loss but produce a net gain. The math is technically accurate. What is missing from the calculation is the adjustment for the quality of the decision being made. A trade taken at twice normal size in a post-loss emotional state is not the same trade as a two-percent position taken from a position of calm evaluation. The entry is less precise, the stop placement is less disciplined, and the management through the trade will be more emotionally reactive. The result is that the theoretical two-percent gain scenario is substantially less likely than the model suggests, while the scenario in which the position reaches its stop at twice the normal loss is just as likely as it would be for any other trade — and is experienced at double the financial and emotional intensity.

A single escalated revenge trade that stops out can produce a session loss that takes days of normal trading to recover. Two in a row can produce a drawdown that takes weeks. Three in a single session — which is not uncommon when the spiral is active — can produce the kind of account damage that some traders never fully recover from, not because the financial loss is necessarily catastrophic but because the damage to confidence and process discipline is severe enough to alter their approach in ways that persist long after the capital is recovered.

3×

The typical session loss multiplier when a revenge trade escalates into a three-loss spiral. A 1% planned drawdown becomes a 3–4% unplanned one within a single hour.

PRACTICAL APPLICATION

Add a single inviolable rule to your trading plan: position size cannot be increased above the standard risk percentage at any point during the same session in which a stop-out has occurred. The rule applies regardless of how compelling the setup appears and regardless of how confident the trader feels. Write it as an absolute constraint rather than a guideline, because the moment it becomes a guideline it becomes negotiable, and the post-loss emotional state is precisely the state in which negotiations are most likely to conclude in favor of the escalation. If a larger position is genuinely warranted by setup quality, it can be taken the following session from a neutral starting position.

TRIGGER CONDITIONS: WHAT MAKES REVENGE TRADES MORE LIKELY

Revenge trades do not occur with equal probability across all loss events. They are significantly more likely under specific conditions, and understanding those conditions is the first step toward building targeted preventions rather than generic willpower-based resolutions.

The loss that felt avoidable is a stronger trigger than the loss that felt inevitable. A trade that stopped out on a late entry, a widened stop, or a deviation from the standard setup criteria creates a specific type of frustration — the trader knows they contributed to the loss through their own execution error. This self-directed frustration is a significantly more powerful driver of revenge trading than the loss that followed a correctly executed setup that simply did not work. The trader who contributed to the loss needs to demonstrate to themselves that the contribution was not characteristic, which makes the next trade an act of self-proof as much as a financial decision.

Multiple losses in a session compound the trigger. A single stop-out generates the impulse but also leaves sufficient emotional resources to manage it. Two consecutive stop-outs substantially increase the probability of a revenge trade, because the emotional weight of the second loss arrives on top of the still-unresolved weight of the first. By the third consecutive loss, the emotional state for most traders has shifted from discomfort to distress, and at the distress level the cognitive resources available for disciplined decision-making are genuinely impaired rather than merely under pressure.

Session context matters as well. A loss on a day when the trader is already under external stress — fatigue, personal pressure, a recent difficult period — arrives with less emotional buffer available to absorb it. A loss late in a session that was previously profitable is experienced differently from a loss early in a session that started flat. The proximity to a round-number account level, a weekly high-water mark, or a personal performance milestone changes the psychological significance of the loss and therefore the intensity of the recovery impulse it generates.

PRACTICAL APPLICATION

Map your own specific revenge trade triggers by reviewing your journal for all instances of trades taken within fifteen minutes of a stop-out. For each instance, note the conditions: how many previous losses in the session, what the emotional quality of the preceding loss was (execution error vs clean stop-out), what time of day it occurred, and whether any external stressors were present. Most traders find two or three highly specific trigger conditions that account for the majority of their revenge trades. Knowing these specific conditions allows for targeted preventions — a mandatory pause after the second consecutive loss, for example — rather than a general resolution to trade better that is too abstract to be reliably acted on under pressure.

WHY WILLPOWER ALONE DOES NOT WORK

The standard prescription for revenge trading is a variant of “just don’t do it.” Recognize the impulse, take a breath, walk away from the screen, and return when calm. This advice is not wrong in principle. Its failure is not in its direction but in its mechanism. It relies on the availability of cognitive and emotional resources at precisely the moment when those resources are most depleted. The post-loss state is not a state of full cognitive availability with a slight emotional disturbance. It is a state in which the very faculties required to evaluate the advice — deliberate reasoning, impulse control, perspective-taking — are operating at reduced capacity.

The neuroscience of this is reasonably well established. Financial losses activate the same threat-response circuitry that processes physical danger. The response is fast, automatic, and prioritizes immediate action over deliberate evaluation. The impulse to act — to trade, to recover, to demonstrate capability — is not a considered choice that can be countermanded by a considered counterchoice. It is a rapid, reflexive response to a perceived threat that arrives before the deliberate reasoning system has time to evaluate it. Willpower, which operates in the deliberate reasoning system, is the wrong tool for the job.

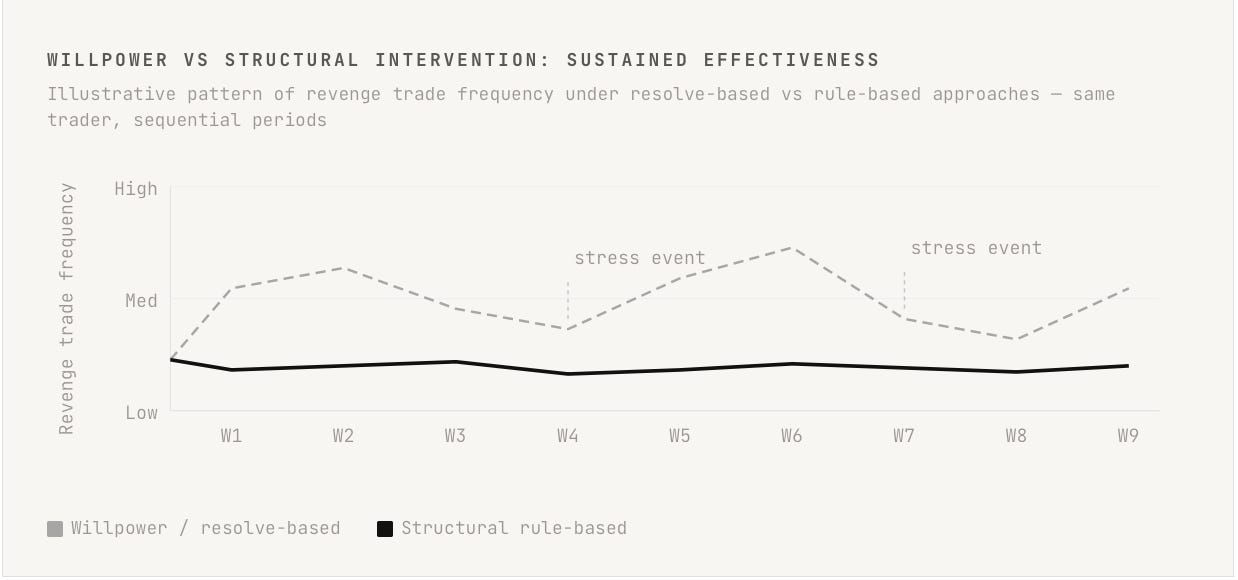

This is why structural interventions work when willpower-based resolutions consistently fail. A structural intervention removes the decision entirely or makes the problematic action physically impossible rather than requiring the trader to resist it under duress. The rule that says no new trades for twenty minutes after a stop-out does not require willpower in the moment. The decision was made in advance, at a time of full cognitive availability, and the rule’s enforcement requires only that the trader not actively override it — a much lower bar than actively resisting a powerful impulse in real time.

PRACTICAL APPLICATION

Audit the approaches you have previously tried for managing revenge trading. If they were primarily resolution-based — deciding to be more disciplined, reminding yourself of the cost, committing to better behavior — note how long each approach held before the next significant drawdown produced a relapse. Then design one structural intervention that removes the decision rather than requiring you to make a better one. The mandatory post-loss pause, the same-session size cap, the platform closure protocol — any of these are structural in the relevant sense. Implement one, track its effectiveness, and compare the frequency and cost of revenge trades during the structural period to the periods of resolve-based management that preceded it.

STRUCTURAL INTERVENTIONS THAT ACTUALLY WORK

The structural interventions that most reliably prevent revenge trading share a common property: they remove the decision from the post-loss emotional state and place it in a pre-committed protocol that was designed in the pre-loss state of full cognitive availability. Each intervention described below has a specific mechanism and a specific scope. None of them requires willpower in the moment of the impulse. All of them require only that the trader not actively override a rule they themselves designed.

The mandatory pause protocol is the simplest and most broadly applicable. After any stop-out, a defined period — typically ten to thirty minutes — must elapse before any new position can be entered. The duration is set in advance based on the trader’s specific pattern: traders who tend to re-enter within two minutes need a longer pause than traders whose impulse peaks later. During the pause, the trader is permitted to watch the market but not to trade. This single intervention breaks the immediate re-entry pattern without requiring any evaluation of the specific trade being considered.

The daily loss limit with session termination is more aggressive and more effective for traders whose revenge trading tends to spiral across multiple trades. When total session losses reach a defined threshold — typically one and a half to two times the standard single-trade risk — the session ends. No more trades are taken regardless of what setups appear. The platform can be closed or the trader can step away, but no new positions are opened for the remainder of the session. This intervention addresses not just the immediate re-entry but the escalating spiral that second and third revenge trades produce.

The post-loss checklist is a procedural intervention rather than a time-based or loss-based one. Before any trade taken after a stop-out, the trader must complete a written checklist that asks: how long since the last loss, is this setup meeting all criteria as written, what is the structural reason for the stop location, and would I take this trade if no loss had occurred today. The checklist does not prevent the trader from taking the trade. It introduces a mandatory deliberation step that forces engagement with the deliberate reasoning system before the trade is entered, which disrupts the fast automatic pathway that produces the revenge impulse without requiring any willpower to resist it.

PRACTICAL APPLICATION

Choose one structural intervention and implement it fully before the next trading session. Write it into your trading plan as a non-negotiable rule with a specific violation consequence — for example, if the mandatory pause is violated, the position must be closed immediately regardless of whether it is winning or losing. The violation consequence is not punitive. It is the mechanism that maintains the structural integrity of the rule when the temptation to override it is at its peak. Review compliance with the intervention weekly alongside your process score, and treat any violation as a process failure independent of the trade’s outcome.

THE DEEPER PATTERN: WHAT REVENGE TRADING REVEALS

Beyond the specific behavioral problem, the revenge trade reveals something important about a trader’s relationship with their strategy and with uncertainty. A trader who consistently takes revenge trades is, at some level, operating with the belief that a loss is a problem to be solved rather than a sample to be incorporated. This belief is understandable — losses feel like problems, and the most immediate available action to address the problem is to trade — but it reflects a fundamental misalignment between the emotional framework being applied and the probabilistic reality of trading.

A strategy with genuine edge will produce a specific distribution of outcomes over a large sample. Within that distribution, losses are not errors. They are part of the expected structure of the system’s behavior. A loss that followed a correctly executed setup is not a problem that needs to be corrected. It is a sample from a distribution that will, over enough repetitions, produce positive expectancy. The trade that follows it is not an opportunity to correct the previous result — market outcomes do not have memory and cannot be corrected — it is an independent sample from the same distribution. Its probability of winning or losing is unchanged by what the preceding sample produced.

The trader who has genuinely internalized this does not experience the loss as a problem demanding immediate resolution. They experience it as information about variance, note it in the journal, and evaluate the next available setup on its own merits. The transition from the first experience to the second is not primarily a behavioral change. It is a conceptual change — a genuine revision in how the loss is interpreted — and it is the most durable foundation for eliminating revenge trading, because it removes the emotional fuel that structural interventions merely contain.

PRACTICAL APPLICATION

After the next correctly executed trade that stops out, write one sentence in your journal before closing the platform: “This loss was a sample from the expected distribution of my strategy and requires no corrective action.” Write it every time, without exception, for thirty consecutive correctly executed losses. The act of writing it is not primarily about the sentence’s content. It is about interrupting the automatic interpretation of the loss as a problem demanding immediate response, and replacing it with a deliberate interpretation that is statistically accurate. After thirty repetitions, the deliberate interpretation begins to become habitual, and the urgency that fuels revenge trading begins, gradually, to reduce.

CONCLUSION

The revenge trade is not a character flaw. It is a predictable output of psychological mechanisms that operate in all human beings and that are specifically activated by financial loss. Understanding it as a mechanical process rather than a moral failure changes the approach to managing it. Character-based approaches — resolving to be more disciplined, reminding oneself of the cost, committing to better behavior — address the wrong level of the problem. Structural approaches — mandatory pauses, session loss limits, pre-trade checklists — address the correct level by removing the decision from the emotional state that produces bad decisions rather than requiring the trader to make good decisions under precisely the conditions that produce bad ones.

The data on revenge trading is consistent across traders, markets, and experience levels: post-loss trades underperform baseline trades on every meaningful metric. Lower win rate, lower average R, higher average loss, lower process scores. The underperformance is not marginal. For most traders who track it honestly, the post-loss period accounts for a disproportionate share of total annual losses. Eliminating or substantially reducing revenge trading is, for many traders, the single highest-return behavioral improvement available — higher return than any refinement to entry criteria, exit rules, or market analysis, because it addresses a cost that is currently being paid in full and that structural changes can reduce to near zero.

The conceptual shift that underlies durable improvement is the revision of what a loss means. Not a problem to be solved. Not a signal that something is wrong. Not an injustice to be corrected. A sample from a distribution that is behaving exactly as a system with genuine edge is expected to behave. When that revision is genuine rather than performative, the urgency that drives the revenge trade has nothing to attach to. The structural interventions remain in place as safeguards. But the primary driver of the behavior — the experience of a loss as a problem demanding immediate resolution — has been removed at the source.

The market did not do anything to you. It produced a sample from a distribution. The trade that follows it has no knowledge of what came before, no obligation to provide recovery, and no special probability of winning because you need it to.