The Patience Problem: Why Waiting for the Right Setup Costs More Than You Think

Patience is described as a virtue in trading so frequently that the description has lost its meaning.

Every trader knows they should wait for the right setup. Most traders cannot. The gap between knowing and doing is not a knowledge problem. It is a structural problem — one that willpower addresses poorly and written process addresses well.

The cost of impatience in trading is direct and measurable. Every trade taken outside the strategy’s defined criteria is a sample drawn from a different distribution than the one the strategy was designed to exploit. That sample may win or lose in any individual instance, but over a large number of such trades it will produce worse expectancy than the on-criteria trades, because the criteria were designed precisely to identify the situations where the strategy’s edge is present. A trade taken because the session has been quiet and something needs to happen is not a setup. It is an activity substitute, and it costs money with the reliability of a tax.

What makes the patience problem genuinely difficult is that it operates through mechanisms that are not experienced as impatience. The trader who enters a marginally qualifying setup does not feel impatient. They feel like they are exercising judgment. The trader who takes a trade on an instrument outside the watchlist because it is moving strongly does not feel like they are abandoning discipline. They feel like they are being opportunistic. The emotional language available for these decisions is almost entirely positive — judgment, opportunism, adaptability — and it conceals the behavioral reality, which is that the entry criteria have been relaxed in response to the discomfort of inaction.

This newsletter is about what generates that discomfort, how it manifests in the specific decisions that reduce expectancy, what the data shows about the cost of impatience across different forms it takes, and what structural interventions consistently reduce its frequency more reliably than resolution alone.

[Download the full printable PDF below.]

WHY DOING NOTHING FEELS WRONG

The discomfort of inaction in trading is not irrational. It is a predictable response to a specific set of features that the trading environment shares with environments in which inaction is genuinely costly. Markets move continuously. Every moment of non-participation has a visible opportunity cost — the price action that occurred while no position was held, the move that was missed, the setup that looked obvious in retrospect. The continuous visibility of these opportunity costs creates a persistent low-level pressure toward action that is absent in most other skilled activities.

The brain’s reward circuitry treats market participation as a form of environmental engagement with real consequences, and disengagement — sitting on the sidelines watching price move without a position — activates the same mild aversion that disengagement from any consequential environment produces. This aversion is entirely independent of whether participation would actually be profitable. The discomfort of watching a market move without a position is not a signal that a good trade is being missed. It is a signal that the environment is producing stimulation that the trader is not responding to. Those are very different things, and trading skill, in part, consists of developing the ability to distinguish them reliably.

The problem is compounded by the structure of most trading sessions. Long periods of low-quality setups punctuated by brief periods of genuine opportunity are the norm rather than the exception. The skill of waiting requires tolerating the low-quality periods without taking action, which means tolerating the discomfort of inaction for extended stretches while the market produces conditions that do not match the strategy’s criteria. That tolerance is a genuine psychological skill, not simply an absence of bad behavior, and it is one that most traders never explicitly develop because it is never framed as something that needs to be trained.

PRACTICAL APPLICATION

For the next two weeks, log every period of ten or more consecutive minutes during a trading session when you felt the urge to trade but did not. Record the time, the approximate emotional quality of the urge — boredom, anxiety, frustration, FOMO — and what the market was doing at that moment. At the end of two weeks, review the log and identify which emotional state most frequently precedes your impatient entries. The specific emotional trigger varies meaningfully between traders. Knowing yours precisely is the first step toward building a targeted intervention rather than applying a general patience prescription that does not address the specific mechanism driving the behavior.

THE FOUR FORMS IMPATIENCE TAKES IN ACTIVE TRADING

Impatience in trading manifests in at least four recognizable forms, each with a distinct mechanism and a distinct cost profile. Identifying which forms are most active in a specific trader’s behavior is necessary for designing interventions that address the actual problem rather than the general category.

The first is early entry — taking a position before the trigger condition is fully met, typically justified by the reasoning that the trigger is clearly going to occur and entering slightly early improves the risk-reward. This form is the most technically sophisticated-feeling variant of impatience because it is framed as precision rather than imprecision. In practice, early entries have lower win rates than entries that waited for the full trigger, for a straightforward reason: the trigger condition exists because the market’s behavior at that specific point provides the statistical evidence the strategy requires. Entering before that evidence arrives is entering on the prediction that the evidence will arrive, which is a lower-quality signal than the evidence itself.

The second form is criteria relaxation — taking a setup that meets most but not all of the strategy’s criteria, typically during a slow period when no fully qualifying setup has appeared for an extended time. This is the most common form and the hardest to catch in real time because the deviation from criteria is small enough to be rationalized as minor. The cumulative cost of criteria relaxation across a large sample is not minor. A setup that meets four of five criteria is not the same trade as a setup that meets five of five. The missing criterion existed in the strategy because it carries predictive value, and its absence reduces the quality of the sample being taken.

The third form is watchlist abandonment — taking a trade on an instrument that was not on the pre-session watchlist because it appears to be offering a good setup in real time. This was addressed in the watchlist newsletter, but it deserves mention here as a form of impatience: the trader has been waiting on their watchlist names and none of them have triggered, so when something else begins moving they redirect attention to it. The pre-session filtering process exists precisely to prevent this redirect, and abandoning it in response to the discomfort of a quiet session on the watchlist names undermines its entire function.

The fourth form is overtrading — taking an excess number of trades beyond the strategy’s natural frequency in a given period, typically because the daily or weekly trade count feels too low relative to what the trader believes they should be doing. Overtrading is the most statistically clear form of impatience because its cost is directly visible in the data: average expectancy per trade declines as trade frequency increases beyond the strategy’s optimal rate, because the marginal setup added by overtrading is always lower quality than the setups that would have been taken under natural frequency.

PRACTICAL APPLICATION

Tag every trade in your journal for the next month with one of four labels: clean entry, early entry, criteria relaxation, or watchlist deviation. At month end, calculate average R separately for each category. The gap between clean entries and each of the three impatience categories represents the direct cost of that specific form of impatience in your own account. For most traders, this analysis reveals that one or two specific forms account for the majority of impatience-related losses, which allows targeted structural responses rather than a general resolution to be more patient that addresses none of the specific mechanisms involved.

WHAT THE DATA SHOWS: THE EXPECTANCY COST OF IMPATIENT TRADES

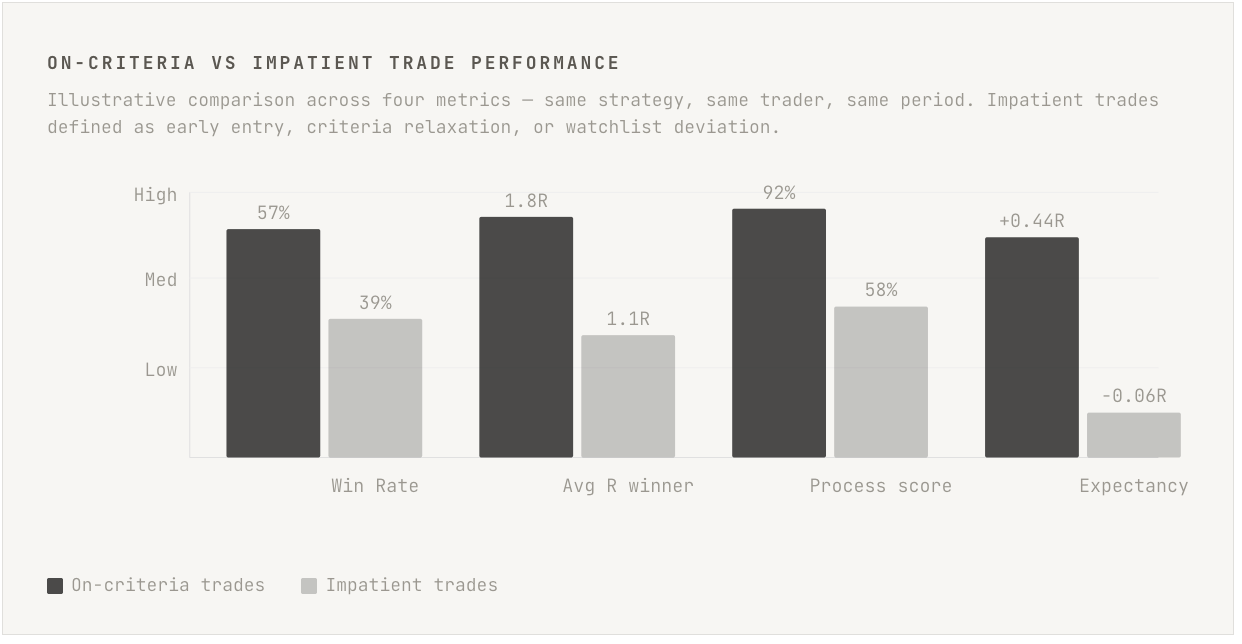

The expectancy cost of impatient trades is consistently underestimated because traders who have not rigorously tracked the distinction between on-criteria and off-criteria trades have no empirical basis for how large the cost actually is. The underestimation is also driven by the same selective memory bias that affects revenge trade tracking: the impatient trades that happened to work are remembered as confirmation that the judgment was sound, while the impatient trades that lost are remembered as unlucky rather than as predictable products of reduced setup quality.

When the data is tracked honestly, the pattern is consistent: impatient trades — however defined — underperform on-criteria trades on every meaningful metric. Win rate is lower. Average R per winner is lower, because the entry quality that determines how much room the trade has to the target before the risk level is reached is compromised by the early or criteria-relaxed entry. Average R per loser is larger in absolute terms, because the structural invalidation level for a marginally qualifying setup is typically less well-defined than for a fully qualifying one, producing less precise stop placement and larger average losses. The combination of lower win rate and worse win-to-loss ratio produces significantly lower expectancy per trade — often negative expectancy — for the impatient category.

The secondary cost is equally significant. Every impatient trade consumes capital, attention, and emotional bandwidth that is no longer available for the on-criteria trade that may appear shortly afterward. A trader who takes a marginally qualifying setup and stops out has not just lost the risk on that trade. They have also reduced their psychological capacity for the next decision, increased the probability of a reactive follow-up trade, and potentially exceeded their session loss threshold in a way that prevents them from taking a genuinely strong setup that appears later in the session. The opportunity cost of impatient trades is real but invisible in the journal, which means most traders who track the direct cost are still underestimating the total cost.

PRACTICAL APPLICATION

Calculate the total P&L impact of your impatient trades over the last six months. Multiply the average R difference between your on-criteria and off-criteria trades by the number of off-criteria trades in that period, then multiply by your average risk per trade in dollars. This number is the direct financial cost of impatience over six months. For most traders who complete this calculation honestly, the number is large enough to be immediately motivating — not as a source of regret, but as a concrete demonstration that patience is not a general virtue but a specific, measurable financial skill with a computable annual value.

FOMO AS A DISTINCT MECHANISM

Fear of missing out — FOMO — deserves separate treatment because it operates through a mechanism that is meaningfully different from general impatience, and the interventions that address general impatience do not fully address it. General impatience is driven by the discomfort of inaction in a stimulating environment. FOMO is driven by the specific perception that a particular opportunity is being missed right now, and that the cost of not acting is a concrete, visible, and irreversible loss of something valuable.

FOMO-driven entries have a specific signature in the data. They tend to occur after a significant move has already begun — the trader has been watching and waiting, the price has moved without them, and the decision to enter is driven by the desire to participate in the remainder of the move rather than by a genuinely favorable entry point. The risk-reward on a FOMO entry is almost always worse than on a timely entry, because the entry is made at a price that is further from the structural support for the stop and closer to where the move’s natural target or resistance is likely to be. The trader is entering the trade closest to the point where a well-managed position would be thinking about reducing or exiting.

The FOMO entry also tends to be made without a clearly defined invalidation level, because the move that prompted the entry has already displaced the obvious technical levels and the trader has not had time to identify the new structural framework. A trade entered without a clearly defined stop is not a trade with a loose stop. It is a trade being managed in real time by a reactive process rather than a pre-committed one, which means the exit decision will be made under emotional conditions rather than structural ones. The combination of a poor entry price, an undefined invalidation level, and real-time reactive management under FOMO conditions is one of the most reliable generators of large individual losses in active trading.

“A move you missed is information about the market. It is not an invitation to participate at a worse price. The setup that was valid at the beginning of the move is not the same setup at the middle of it.”

PRACTICAL APPLICATION

Implement a FOMO check as a mandatory step before any entry that was not on the pre-session watchlist or that was not triggered by the planned scenario. The check asks three questions: has this instrument already moved more than fifty percent of its average daily range before this entry, is there a clearly defined structural level for stop placement that existed before the move began, and would I have taken this trade at this price if I had been watching it from the session open? A no to any of the three questions is a hard pass. The first question alone eliminates the majority of FOMO-driven entries, because most of them occur after a meaningful portion of the available move has already occurred.

THE OVERTRADING TRAP: WHEN ACTIVITY REPLACES EDGE

Overtrading is the form of impatience most directly visible in the aggregate data, and it is the one most commonly misidentified as something else. A trader whose strategy generates ten to fifteen setups per month but who is consistently taking thirty to forty trades is not operating a modified version of their strategy. They are operating a different strategy with worse parameters, and they are doing so without having designed, tested, or validated it.

The mechanism behind overtrading is a cognitive error about what trading activity represents. Traders who are working hard on their process, spending significant time preparing and analyzing, develop a sense that the output of that effort should be proportional to the input. When the strategy only produces ten setups in a month, it feels like the preparation generated insufficient return on the time invested. The uncomfortable conclusion — that waiting is the work, and that a ten-trade month with high average R is vastly preferable to a forty-trade month with low or negative average R — runs counter to a deeply held intuition that more activity is more productive.

The statistical cost of overtrading is direct. Every trade beyond the strategy’s natural frequency is, by definition, a trade taken in conditions that did not meet the full criteria — because if they had met the full criteria, the strategy would have identified them as setups within its natural frequency. These marginal trades reduce the session’s average expectancy because they add negative-expectancy samples to a distribution that was positive-expectancy without them. Over a full year, a trader who overtrades by a factor of two or three is producing significantly worse risk-adjusted returns than they would have produced from a fraction of the trading activity, which means their actual trading is destroying value that their correct setups are creating.

PRACTICAL APPLICATION

Calculate your strategy’s natural frequency: the number of fully on-criteria trades generated per week or per month based on your historical data. Set a soft ceiling at one and a half times that number. When the current period’s trade count approaches that ceiling, conduct a brief review of the remaining trades before taking them. Are they meeting all criteria, or are some of them marginal qualifications that feel compelling because the period’s count has been low? The ceiling is not a hard rule that prevents good trades from being taken. It is a trigger for increased scrutiny at the point in the session or week when the probability of impatient entries is highest.

SESSION STRUCTURE AND THE PATIENCE ARCHITECTURE

One of the most effective structural responses to the patience problem is not behavioral at all. It is architectural — the design of the trading session in ways that reduce the conditions under which impatient entries are most likely to occur, rather than relying on in-session willpower to resist them after those conditions have already been generated.

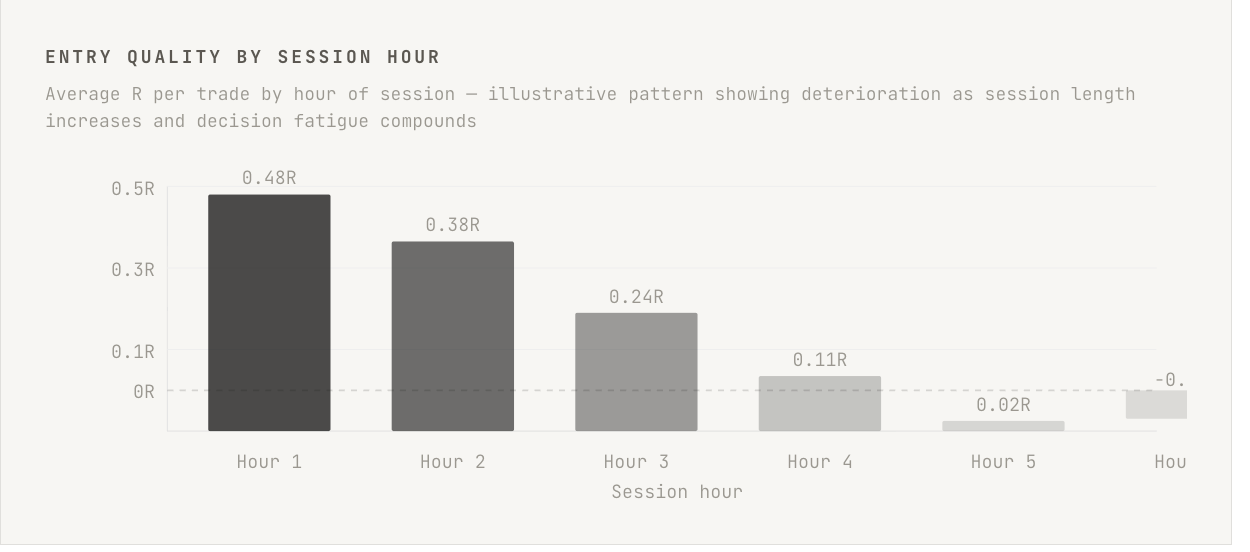

Session length management is the most underused tool in this category. Patience erodes over time within a session. The first hour of a session, for most traders, is characterized by relatively high selectivity and clear-headed evaluation. By the third and fourth hour, even traders with strong process discipline show measurable increases in criteria relaxation and marginally qualifying entries. The longer the session, the more the compounding effect of decision fatigue, missed opportunities, and accumulated stimulation degrades the quality of the entry filter. A trader who limits active session duration to the periods when their historical data shows the best performance is not leaving opportunities on the table. They are eliminating the low-quality decision period that those additional hours represent.

Pre-session scenario clarity also reduces in-session impatience by a mechanism that is easy to overlook. A trader who arrives at the session with precisely written scenarios — specific levels, specific trigger conditions, specific invalidations — has fewer decisions to make in real time. The in-session experience is less one of evaluating whether to act and more one of monitoring whether predefined conditions are met. This shift from evaluation mode to monitoring mode is significant: evaluation requires active decision-making under stimulation, which is the condition that produces impatient entries. Monitoring requires only comparison against a written reference, which is substantially more resistant to impatient deviation.

PRACTICAL APPLICATION

Segment your trade journal by session hour and calculate average R for each hour segment. Identify the hour at which your average R first falls below half of your first-hour average. That hour is your optimal session end time — the point at which continued participation is generating significantly lower value per trade than the earlier part of the session. Implement a soft session end at that time as a default, with any extension requiring explicit justification based on a specific setup that was on the pre-session watchlist and has not yet triggered. Most traders who run this analysis find that their optimal session length is shorter than their typical session length by one to two hours.

WHY STRUCTURAL CONSTRAINTS OUTPERFORM RESOLUTION

The pattern described throughout this newsletter — knowing that patience is valuable, resolving to be more patient, failing to maintain that resolution under the specific emotional conditions that generate impatience — is the standard arc of willpower-based approaches to behavioral problems in trading. It is not that resolution is useless. It is that resolution applied without structural support degrades predictably under the specific conditions where it is most needed: long quiet sessions, consecutive missed setups, periods where the market is moving but not in ways the strategy can exploit.

A structural constraint does not require the trader to feel patient. It requires only that they not actively override a pre-committed rule. This distinction is everything. The mandatory waiting period between a watchlist depletion and a non-watchlist entry does not demand psychological resources from the trader during the moment of temptation. The trade count ceiling does not require resistance to a compelling-looking marginal setup. The session end time does not require the trader to convince themselves that the fifth hour has been less productive than the first two. Each structural constraint removes a decision from the moment when the emotional conditions for making it well are most compromised.

The most effective structural constraints for patience specifically are time-based rather than outcome-based. A rule that says no new entries in the last ninety minutes of the session is easier to follow than a rule that says stop trading when your entries are getting worse, because the first requires only clock-reading while the second requires real-time assessment of one’s own decision quality under conditions of decision fatigue. The assessment that would be needed to trigger the outcome-based rule is precisely the type of assessment that decision fatigue impairs. The time-based rule requires no such assessment and is therefore reliable across the full range of psychological states that a trading session produces.

PRACTICAL APPLICATION

Implement two time-based structural constraints before the next trading week. First, define the session hours during which you will actively trade, based on your historical performance by hour. Outside those hours, the platform can be open for monitoring but no new positions will be initiated. Second, define a minimum time gap between consecutive entries — for example, no new position within thirty minutes of the previous entry closing, unless the new entry was on the pre-session watchlist and its trigger fires within the natural timeframe of the scenario. Write both constraints into your trading plan. Review compliance weekly as part of the process audit. Violations are process failures regardless of outcome.

REFRAMING PATIENCE: FROM VIRTUE TO COMPETITIVE ADVANTAGE

The framing of patience as a virtue — as something morally admirable that the disciplined trader possesses and the undisciplined one lacks — is not the most useful frame for practical trading. Virtue framing places patience in the category of character, which implies that having it or not is largely fixed and that the prescription for traders who lack it is primarily about developing better character. That is not particularly actionable advice, and it tends to produce the guilt-resolve-relapse cycle that is the hallmark of willpower-based approaches to behavioral problems.

A more useful frame is competitive advantage. In any zero-sum market context, the trader who takes only the highest-quality samples from the available opportunity set and ignores everything else is extracting a more favorable distribution of outcomes than the trader who takes a broader, lower-quality sample. The patient trader is not morally superior. They are tactically superior. Their selectivity is the mechanism by which they access a higher mean and lower variance in their outcome distribution, which compounds into meaningfully better risk-adjusted returns over any extended period. Patience, understood this way, is not a character trait to be cultivated. It is a filter to be maintained — structurally, consistently, and measurably.

This reframing also changes the emotional relationship with quiet sessions and missed setups. A day with no qualifying trades is not a wasted day. It is a day on which the filter functioned correctly and prevented a set of negative-expectancy samples from entering the performance record. It is, in expectancy terms, a day on which the trader made money relative to the counterfactual of taking the trades that did not qualify. The visible opportunity cost — the moves that occurred without a position — is not the relevant comparison. The relevant comparison is the expected outcome of the marginal trades that were not taken, which is negative. Not taking negative-expectancy trades is a positive contribution to long-run performance, even though it feels like nothing happened.

PRACTICAL APPLICATION

At the end of every session in which you did not trade — or traded significantly less than your typical session volume — write one sentence in the journal: “The filter functioned correctly today.” Do not evaluate the market action that occurred without positions. Do not calculate what would have been made if the passed-on setups had been taken at full size. Record only that the process worked as designed, and that the absence of activity was a product of the strategy’s criteria rather than of missed opportunities. After thirty consistent applications of this reframe, the emotional experience of a quiet session will begin to change from frustration to something closer to professional satisfaction. That change, modest as it sounds, reduces the pressure toward impatient activity in subsequent sessions by shifting what the absence of trades feels like.

The patience problem is about the mismatch between the psychological environment that active markets create — continuous stimulation, visible opportunity costs, activity bias — and the behavioral requirements of a strategy that generates positive expectancy by being highly selective about which opportunities it exploits. That mismatch produces impatient behavior not because the trader lacks virtue but because the environment is specifically constructed to make selective inaction uncomfortable, and the trader has not built structural defenses against that discomfort.

The cost of failing to build those defenses is concrete and measurable. Every impatient trade is a sample drawn from a distribution with worse parameters than the strategy’s defined edge. Over a large number of such trades, the cumulative drag on expectancy is significant. For many active traders, eliminating impatient entries is the single change that would most improve their annual risk-adjusted returns, ahead of any refinement to entry signals, exit rules, or market analysis — because it removes a persistent source of negative-expectancy activity that is currently being paid for in real capital.

The interventions that work are structural rather than psychological. Session length limits, mandatory inter-trade gaps, trade count ceilings, FOMO checklists, watchlist commitment rules — each of these removes a specific category of impatient entry from the opportunity set without requiring the trader to make a better decision in the moment. They require only pre-commitment during a period of clear thinking, and compliance monitoring during the weekly review. The difficulty of following them is entirely front-loaded: it requires honest self-assessment about which forms of impatience are most active, and the discipline to write rules that address those forms precisely. Everything after that is monitoring and iteration.

A day with no trades is proof that the filter working. The question is not whether you had the patience to wait — it is whether you had the structure that made waiting the default rather than the exception.