The Anatomy of a Real Setup: What Separates Structure From Pattern Memorization

Most traders think they have setups. What they actually have is a loose collection of visual preferences and gut reactions dressed in the language of a system.

The difference between those two things is the difference between a career and an expensive hobby.

Ask a trader to describe their setup and they will usually tell you something about a chart pattern, a moving average, or a zone they are watching. Ask them to define the exact conditions that must be present before they enter, where their stop goes and why, and what market environment their setup requires to work, and the answer becomes substantially less clear. That lack of clarity is not a minor gap. It is the central problem.

A real setup is not a visual pattern. It is a documented, testable hypothesis about participant behavior, expressed as a precise set of conditions that can be repeated under the same rules and measured over a large sample. Without that precision, the trader is not executing a system. They are reacting to the chart in real time and constructing a post-hoc rationale that sounds systematic but is not.

This newsletter is about what a real setup actually contains, why most traders operate with far less structure than they believe, and what it takes to build something that can generate reliable data about its own performance over time.

A SETUP IS A HYPOTHESIS, NOT A PATTERN

The most important mental shift in setup design is moving from visual recognition to causal reasoning. Pattern recognition asks: does this chart look like a previous chart that worked? Causal reasoning asks: what is happening in this market that creates a temporary inefficiency I can exploit, and under what conditions does that inefficiency reliably resolve in my favor?

These are fundamentally different questions, and they produce fundamentally different systems. A pattern-based approach produces something that can look good in backtests on historical data but fails to generalize because the trader does not understand why it worked in the first place. When the pattern shows up in a different context, or the market structure shifts, there is no framework for evaluating whether the underlying logic still applies. The trader simply takes the trade and hopes the shape still carries the edge it appeared to carry before.

A hypothesis-based approach starts from a specific claim about market behavior. Trend continuation exists because participants adjust their positioning gradually, not instantly, and momentum flows tend to extend further than initial estimates suggest. Mean reversion exists because panic and greed periodically push price too far from equilibrium, and corrective flow eventually overwhelms the directional imbalance. Liquidity sweeps exist because retail stop clusters accumulate at obvious levels, and larger participants systematically exploit that predictability. Each of these is a falsifiable claim about how markets work, and each produces a setup with a clear internal logic that can be evaluated both statistically and analytically.

The practical consequence of this distinction is significant. When a hypothesis-based setup stops performing, the trader can investigate why. Is the market regime no longer one where the underlying behavior occurs? Has the specific inefficiency been arbitraged away? Are the conditions being measured accurately representing what the hypothesis requires? These are answerable questions. “Does the pattern still work” is not, because there is no causal logic underneath it to evaluate.

PRACTICAL APPLICATION

For every setup you currently trade, write a single sentence that completes this prompt: “This setup works because...” If that sentence describes a visual shape, the setup is pattern-based and does not yet have a hypothesis underneath it. If it describes participant behavior, information asymmetry, or a structural market dynamic, the setup has a foundation worth building on. The exercise is more diagnostic than it sounds. Most traders find it genuinely difficult to complete the sentence without defaulting to the visual.

THE TWO LAYERS EVERY SETUP REQUIRES

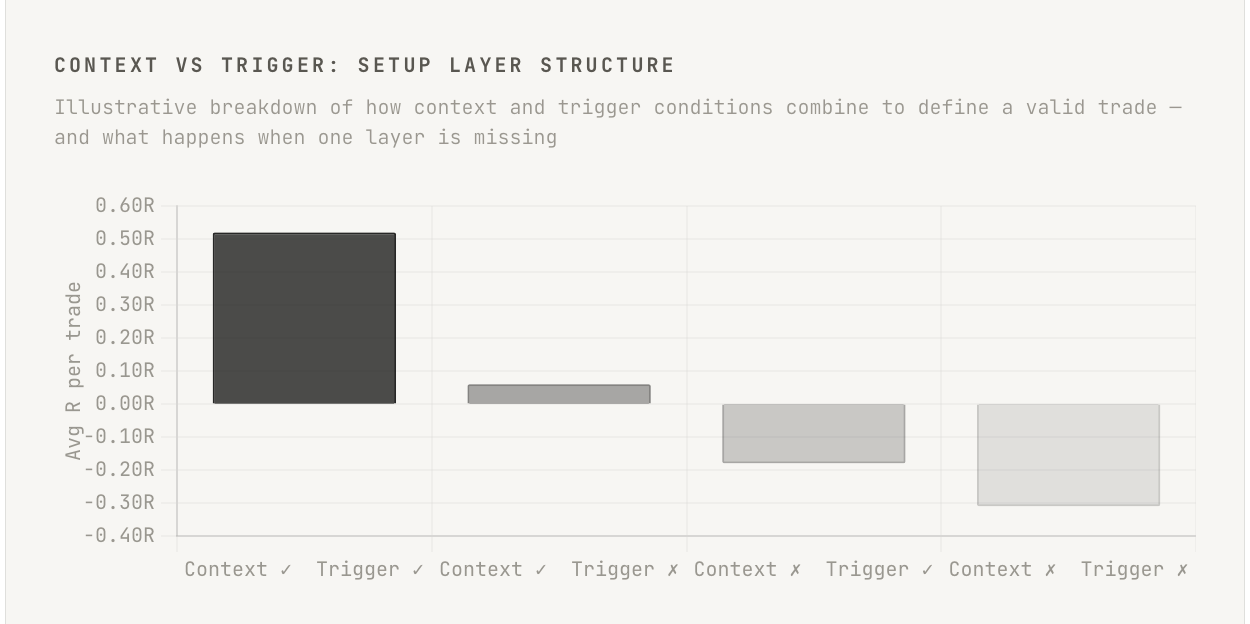

A well-constructed setup always has two distinct layers: context and trigger. These are not the same thing, and confusing them is one of the most common structural errors in setup design. Context defines the environment in which the trade makes sense. Trigger defines the specific condition that causes entry. Both must be present for a trade to be valid. Either one alone is insufficient.

Context operates at a higher timeframe or broader structural level. It answers the question: does the current market environment support the underlying logic of this setup? If you trade momentum continuation, the context layer confirms that a genuine momentum phase is in progress, not a choppy, range-bound market that mimics the visual characteristics of a trend. If you trade mean reversion, the context layer confirms that the market has actually overextended rather than simply moved. Context is what prevents a technically valid trigger from being taken in an environment that structurally opposes it.

Trigger operates at the execution level. It answers the question: given that the context is correct, what specific event or condition causes me to enter right now rather than five minutes ago or five minutes from now? The trigger must be precise enough to be identified without ambiguity, repeatable under the same rules across different sessions, and logically connected to the context rather than independently derived from it. A trigger that exists without context produces entries scattered across all market conditions, many of which the underlying hypothesis does not support.

Most traders operate with only one of the two layers. They have either a strong bias about market direction with no precise execution mechanism, or they have a precise entry signal with no framework for evaluating whether the broader environment supports it. The first produces good analysis and poor timing. The second produces mechanical entries that generate inconsistent results across different market conditions and leave the trader unable to explain why performance varies so dramatically from one period to the next.

PRACTICAL APPLICATION

Write out your current primary setup with the two layers clearly separated. Label everything above the entry decision as context, and everything at the entry decision itself as trigger. If you cannot make that separation cleanly, the setup is not yet sufficiently designed. The separation should be obvious enough that you could hand your written rules to another trader and they would reach the same entry decision in the same market at the same time. If that exercise reveals ambiguity, the ambiguity is where emotional decision-making enters the process.

PRECISION IS NOT OPTIONAL

Vague rules are not a minor inconvenience. They are a structural failure that produces two distinct problems. The first is that vague rules cannot be tested. If your context condition is “the market is trending,” you cannot measure how often that condition correctly identifies profitable environments because the condition itself is not defined precisely enough to apply consistently. Every measurement of its effectiveness will be contaminated by the subjectivity of what counted as a trend on any given day. The second problem is psychological. Vague rules are filled in by whatever the trader is feeling at the moment of execution. Fear and greed do not disappear when a trader builds a system. They simply move into the gaps left by imprecise definitions.

Precision means something specific. It means that every condition in the setup has a measurable, observable definition. “Higher timeframe uptrend” is not precise. “Price above the 50-period EMA on the daily chart with at least two consecutive higher highs and higher lows” is closer to precise. “Strong momentum” is not precise. “A candle closing in the top 20 percent of its range with volume exceeding the 20-period average” is closer. The exact definitions will vary by setup type, market, and timeframe, but the principle holds regardless of specifics: if the condition cannot be identified mechanically and consistently, it is not yet a rule.

2

The number of traders who should reach identical entry decisions given the same market and the same written rules. If they diverge, the rules are not yet precise enough.

There is a specific moment when precision becomes real for a trader. It is when they write a rule, apply it to historical data, and discover that it identifies situations they would not have called the setup when looking at the chart in real time. That discomfort is the precision working correctly. It reveals the gap between what the trader believed they were doing and what the rules actually specify. Closing that gap, resolving it in favor of the precise rule rather than the intuitive read, is where the real work of setup design happens.

PRACTICAL APPLICATION

Take one condition from your primary setup and apply it to the last thirty trading sessions without looking at what the market did afterward. Count how many times the condition triggered. Then review those instances against your actual trade log for the same period. If the condition identifies significantly more or fewer setups than you actually traded, you have direct evidence that the rule as written and the rule as applied are two different things. That discrepancy is quantifiable, and it tells you exactly where the setup needs to be tightened.

INVALIDATION IS PART OF THE SETUP, NOT AN AFTERTHOUGHT

Most traders think about where to place their stop after they have decided to take the trade. This is the wrong order. Invalidation should be defined as part of the setup design itself, before any individual trade is considered. The stop location is not primarily a risk management decision. It is a structural declaration of what market condition would prove the setup’s underlying logic incorrect. The risk management consequence follows from that structural logic, not the other way around.

When invalidation is designed correctly, the stop location emerges directly from the hypothesis. If the setup is based on the idea that a specific level will hold as support and generate continuation, the invalidation point is a clean close below that level. If the setup is based on momentum continuation after a consolidation, the invalidation point is a failure to maintain momentum structure, defined precisely enough to be identified on a chart without ambiguity. The stop is placed where the trade’s underlying reason for existing no longer holds, not at an arbitrary distance from the entry that produces a reward-to-risk ratio the trader finds aesthetically acceptable.

When invalidation is treated as an afterthought, traders make two characteristic errors. The first is placing stops at technically indefensible levels simply because the intended stop location would produce a loss too large relative to the target. This is the risk management tail wagging the structural dog, and it results in trades being stopped out by normal market noise before the setup has had a genuine opportunity to resolve. The second error is widening the stop during the trade when the market approaches the invalidation level, because the trader has not genuinely committed to what would make the setup wrong. Both errors stem from the same source: the invalidation point was never built into the setup at the design stage.

PRACTICAL APPLICATION

For your primary setup, write the invalidation condition before you write the entry condition. Ask: if this trade is wrong, what will the market have done to prove it? Write the answer as a specific, observable market event. Then place your stop at the level that corresponds to that event, and calculate what position size produces one R of risk at that distance. If the resulting position size is too small to be meaningful or the risk is too large for your account, the trade does not fit your parameters. Do not adjust the stop to make the math work. Find a different setup that fits, or pass on the trade.

THE ROLE OF MARKET ENVIRONMENT IN SETUP QUALITY

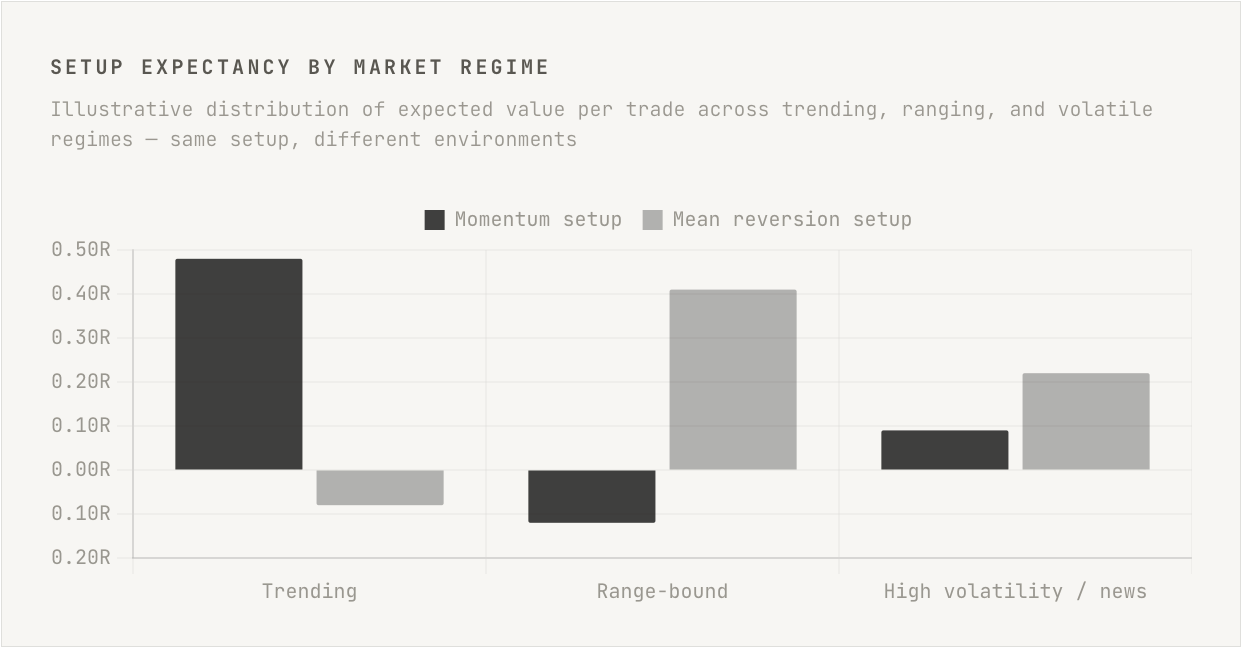

No setup works equally well in all market conditions. This is not a weakness of any particular strategy. It is a mathematical fact about how edges are generated. Every setup exploits a specific type of market behavior, and that behavior occurs with different frequency and reliability depending on the current regime. A momentum setup exploits directional follow-through, which is abundant in trending regimes and nearly absent in range-bound ones. A mean-reversion setup exploits overextension and corrective flow, which dominates in low-volatility, oscillating markets and fails in sustained trending environments where overextension keeps extending.

The practical consequence is that setup quality is not fixed. The same visual pattern carries different expected value depending on the market environment it appears in. Taking a momentum continuation setup during a choppy, news-driven session produces a different expectancy than taking the same setup during a clean directional day. The entry may look identical. The underlying conditions that give the setup its edge are not. Traders who do not account for regime in their setup design are effectively trading a system that has a variable expectancy they are not measuring or accounting for.

“The setup you are trading has a different expected value today than it did last week. Regime is not background noise. It is a primary input.”

Regime awareness does not require a formal model. It requires a set of defined characteristics that describe the environments in which the setup’s underlying logic is most and least likely to hold. For a momentum trader, this might include average daily range relative to recent history, the slope and consistency of a higher timeframe trend, and the presence or absence of major scheduled news risk. For a mean-reversion trader, it might include the distance from a key moving average, implied or realized volatility relative to its recent range, and whether the market has been respecting or violating obvious levels. These characteristics can be assessed before the session begins and used to calibrate whether the setup should be traded at full size, reduced size, or not at all.

PRACTICAL APPLICATION

Define two or three market characteristics that describe the ideal environment for your primary setup. These should be measurable and assessable before each session, not evaluated in hindsight. At the end of each trading week, tag every trade in your journal with the regime conditions that were present at the time of entry. After thirty to fifty tagged trades, review performance by regime category. The data will almost certainly show that a subset of conditions accounts for a disproportionate share of the setup’s total expectancy. That subset is the real setup. The broader set of conditions is a diluted version of it.

EXIT DESIGN IS WHERE MOST SETUPS BREAK DOWN

Traders spend the majority of their setup development time on entries. This is understandable, because the entry is the most visible and psychologically engaging part of the trade. But the entry is not where expectancy is primarily determined. Entry quality sets the initial risk-reward ratio. Exit quality determines what fraction of that potential reward is actually captured across a large sample of trades. A setup with a mediocre entry and a disciplined, well-designed exit structure will consistently outperform one with a precise entry and an emotionally driven exit process.

Exit design has two components: the target structure and the management rules. The target structure defines where the trade is expected to reach, based on the same hypothesis that justifies the entry. If the setup exploits a move from one liquidity zone to the next, the target should be at or before that next zone, not at an arbitrary multiple of the initial risk. If the setup exploits mean reversion from an extreme, the target should be at or near the mean, not extended to capture additional movement beyond it. Targets that are logically derived from the hypothesis will be hit with a frequency that is consistent with the underlying edge. Arbitrary targets will produce an inconsistent hit rate that makes the system’s true expectancy difficult to evaluate.

Management rules govern what happens between entry and the target or stop. They address questions like: at what point, if any, does the stop move to breakeven? Under what conditions, if any, is the target extended? Is there a partial exit structure, and if so, at what level and for what fraction of the position? These rules must be defined in advance and applied consistently. The most common failure mode in exit management is that traders make these decisions in real time, under the emotional influence of whatever the position is doing at that moment. A winning trade approaching the target feels like it should run further. A losing trade approaching the stop feels like it should be given more room. Both instincts, when followed, systematically damage the expectancy of an otherwise sound setup.

PRACTICAL APPLICATION

Review your last fifty closed trades and calculate what the average R outcome would have been if you had simply held every trade to its original target or stop without any discretionary modification. Compare that number to your actual average R. If the actual average is lower than the mechanical average, your discretionary exit decisions are costing you money. The gap between the two numbers is the exact cost of emotional exit management, expressed in R per trade. That number, multiplied across your annual trade count, is the annual cost of the problem. Most traders find the figure large enough to motivate genuinely changing the behavior.

SAMPLE SIZE AND THE ILLUSION OF A TESTED SETUP

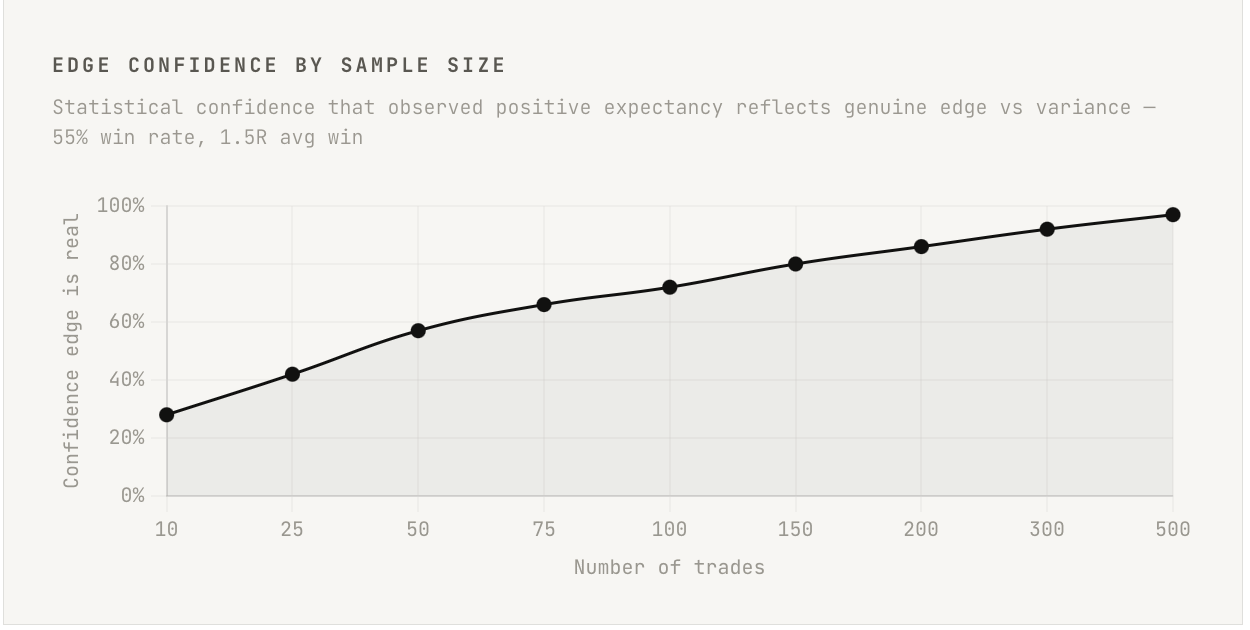

A setup that has produced ten winning trades is not a tested setup. It is a setup with a short and potentially misleading track record. This point is understood at an intellectual level by most traders, but the behavioral implications of it are consistently ignored. Traders routinely increase position size, reduce selectivity, or declare a method validated after sample sizes that provide almost no statistical confidence about whether the edge is real or coincidental.

The mathematics are not generous. A setup with a fifty-five percent win rate and a one-and-a-half-to-one average reward-to-risk ratio, which is a genuinely strong edge, requires approximately two hundred to three hundred trades before the observed performance begins to separate reliably from the range of outcomes that pure chance could produce. At twenty trades per month, that is ten to fifteen months of clean, consistent execution before the data is meaningful. Most traders have neither the patience nor the structural consistency to reach that sample size without modifying the setup multiple times along the way, each modification resetting the sample clock and preventing the accumulation of genuinely useful data.

The solution is not to test for longer before trading. It is to understand what a small sample does and does not tell you, and to make decisions accordingly. A fifty-trade sample can reveal obvious structural flaws in a setup, such as a consistently negative average win relative to average loss, or a win rate dramatically below what the hypothesis would suggest. It cannot reliably confirm that a positive expectancy is real rather than a product of favorable variance. That distinction matters enormously for how a trader interprets early results and makes decisions about whether to continue, modify, or abandon a method.

PRACTICAL APPLICATION

Before trading any new setup with real capital, define the minimum sample size you will collect before making any structural modifications to the rules. Write this number down and commit to it. The number should be at minimum fifty trades, and ideally one hundred or more. During this period, the only permitted action is to document results and maintain clean records. No rule changes, no parameter adjustments, no adding filters because recent results have been poor. The purpose of the sample period is to generate data, not to produce returns. If that distinction is not clearly held, the sample will be contaminated before it is large enough to be useful.

BUILDING THE SETUP INTO A WRITTEN SYSTEM

A setup that exists in a trader’s head is not a system. It is a set of preferences that will be applied inconsistently, modified under pressure, and impossible to evaluate objectively. The act of writing a setup down in complete, precise terms is not administrative overhead. It is the process by which the setup becomes real in a structural sense. What cannot be written cannot be tested. What cannot be tested cannot be improved. What cannot be improved will not survive contact with a sustained drawdown period or a significant regime shift.

A written setup document should include the underlying hypothesis in plain language, the specific context conditions and how each is measured, the specific trigger conditions and how each is identified, the exact invalidation point and the logic behind it, the target structure and how targets are derived, the management rules for every discretionary decision that might arise between entry and close, and the regime conditions under which the setup will and will not be traded. Every item on that list should be specific enough that a trader who has never seen your charts could apply the rules to a new market and reach the same decisions you would reach.

The process of writing a setup reveals its weaknesses faster than trading it live does. Gaps that feel resolved when held loosely in the mind become obvious the moment they must be expressed in precise language. This is why many traders resist writing their rules down completely. The imprecision is comfortable because it preserves optionality. Every time a rule is left vague, the trader retains the ability to interpret it however feels right in the moment. That optionality feels like flexibility but functions as a mechanism for emotional decision-making to contaminate a process that should be statistical.

PRACTICAL APPLICATION

Write your primary setup as a complete document using the structure described above. When finished, hand it to someone who understands markets but is unfamiliar with your specific approach, and ask them to identify the first point at which the rules become ambiguous. That point is your first edit. Repeat the process until the document produces no ambiguities. The resulting document is your trading plan for that setup, and it becomes the reference against which every execution is evaluated. A trade that follows the plan is a good trade regardless of outcome. A trade that departs from the plan is a process failure regardless of outcome. That distinction, applied consistently, is what transforms a setup into something that can be managed, measured, and genuinely improved over time.

CONCLUSION

The gap between a trader who has a setup and a trader who has a real setup is a gap in structural precision. Both traders may have identified the same general opportunity in the market. One has expressed that opportunity as a documented, testable, repeatable system with a clear hypothesis, defined conditions, structured exits, and a framework for evaluating performance. The other has expressed it as a general preference that is applied with variable consistency and interpreted differently depending on how the most recent trades resolved.

The practical consequences of that gap compound over time. The trader with a real setup accumulates data that can be analyzed and used to make genuine improvements. Their edge, if it exists, becomes clearer with each passing month. Their weaknesses, if they exist in the setup design, can be identified and corrected. The trader without a real setup accumulates experience but not information, because the inconsistency of execution means the outcomes do not reliably reflect the performance of any specific method. They improve slowly if at all, and they remain vulnerable to the behavioral pressures that every drawdown produces, because there is no precise reference point against which to evaluate whether their execution is sound.

Building a real setup takes longer than finding a pattern that works for a few weeks. It requires the uncomfortable discipline of writing rules precisely enough that they eliminate the comfortable vagueness most traders rely on. It requires collecting sample sizes large enough to generate meaningful data before drawing conclusions. It requires defining invalidation as a structural concept rather than a risk management afterthought. None of this is beyond the reach of a serious trader. All of it requires a level of rigor that most traders never apply, which is precisely why the edge it produces is real.

A setup becomes real the moment it can be evaluated objectively. Until then, it is just a story you tell yourself about why you took the trade.