How to Review Your Trades Without Lying to Yourself

Most traders review their trades the way most people assess their own driving — they conclude they are above average, their mistakes were situational, and their successes were the product of skill. The journal becomes a document that confirms what the trader already believes rather than one that reveals what is actually happening.

This is not a character flaw. It is a structural problem. A review process that produces biased conclusions does so because it is designed, usually unintentionally, to allow bias in. The trader reviews outcomes rather than decisions. They remember what happened differently from how it actually occurred. They apply different standards of scrutiny to winning trades and losing trades. They focus on the trades that stand out rather than on the statistical patterns that only appear across a large sample. Each of these tendencies has a predictable direction, and that direction is always toward flattering the trader’s self-image at the expense of accurate diagnosis.

An honest review process is not one that makes the trader feel worse about their trading. It is one that produces information accurate enough to support genuine improvement. The difference between the two is structural. The honest review is built on specific rules about what gets recorded, when it gets recorded, how decisions are evaluated, and how patterns are identified. Those rules exist precisely to prevent the biases that feel natural from contaminating the conclusions that actually matter.

This newsletter builds that structure from the ground up — what to record, how to evaluate it, what patterns to look for, and how to convert a review session into decisions that actually change behavior going forward.

[Download the full printable PDF below.]

WHY MOST TRADE REVIEWS PRODUCE NOTHING USEFUL

The failure mode of a typical trade review is not that the trader is lazy or dishonest. It is that the review is conducted using the wrong data, in the wrong order, with the wrong focus. The most common version looks like this: the trader opens their platform at the end of the session, looks at the P&L, scans through the day’s trades, identifies one or two that stand out, forms an opinion about why the day went the way it did, and closes the platform. This is not a review. It is a rationalization session with charts.

The fundamental problem is that outcome-driven review is contaminated by hindsight from the moment it begins. When the trader already knows that a trade lost money, they evaluate the entry differently than they would have if the outcome were unknown. Details that were invisible during execution become obvious in retrospect. The decision looks worse than it actually was because the trader is evaluating it through the lens of what subsequently happened rather than through the information that was actually available at the time the decision was made.

The second problem is selective attention. Traders naturally focus on the trades that produced strong emotions — the big wins, the painful losses, the near-misses. These are not the trades that contain the most useful information about the system’s performance. Statistically, the most informative trades are the unremarkable ones: the trades that were taken cleanly, followed the plan, and produced ordinary results. The pattern of ordinary results across a large sample tells you far more about the health of the strategy than any individual dramatic outcome.

The third problem is the absence of a counterfactual record. A trader who only records trades they took has no information about the trades they passed on. If the passed-on setups would have won at a higher rate than the taken setups, the filtering process is adding negative value. Without a record of what was seen and passed on, none of this is visible.

PRACTICAL APPLICATION

Before the next review session, write down in one sentence what you believe is currently the biggest weakness in your trading. Seal it or set it aside. Conduct the review using the structured process described in this newsletter. At the end, compare what the data shows to what you predicted. The gap between the two is a direct measure of how much your self-assessment diverges from your actual performance — and that gap is the starting point for building a review process that produces honest conclusions rather than comfortable ones.

RECORDING BEFORE KNOWING: THE CORE DISCIPLINE

The single most important structural rule in an honest review process is that the majority of what gets recorded must be recorded before the outcome is known. This is the discipline that separates a journal from a log. A log records what happened. A journal records what the trader was thinking and deciding while it was happening, before the market delivered its verdict on those decisions.

In practice this means recording at minimum three things before entry: the setup conditions that qualified the trade, the specific level or zone being used as the stop, and the scenario — the sequence of events that would need to occur for the trade to reach the target. These three elements define the trade’s logic completely and independently of its outcome. If they are recorded before entry, the post-trade review can evaluate whether the logic was sound without the outcome contaminating the assessment.

During the trade, the one additional record that matters is any management decision that deviates from the original plan. If the stop is moved, write why at the moment of moving it. If a partial exit is taken outside the original management rules, write the reason immediately. These in-trade records are the most revealing data in the entire journal, because they capture the trader’s thinking at the exact moment when emotional pressure is highest and reasoning quality is most likely to degrade.

After the trade closes, the only thing that needs to be added is the result in R and a brief factual description of how the trade resolved. The explanatory analysis — why it worked or did not — should be deferred until the weekly review rather than written immediately after close, because the emotional state immediately following a trade outcome produces some of the most consistently biased post-trade writing in any journal.

PRACTICAL APPLICATION

Create a pre-entry record template with exactly four fields: setup conditions met (checklist, yes or no for each rule), stop level and structural reason for it, target level and structural reason for it, and scenario — one sentence describing what the market needs to do for this trade to work. Complete all four fields before placing the order. After one month of consistent pre-entry recording, you will have a dataset that allows genuine evaluation of your decisions rather than your outcomes — and the two will not look the same.

THE PROCESS SCORE: SEPARATING EXECUTION FROM OUTCOME

The most practically useful addition to any trade journal is a process score — a numerical rating of how well the trader followed the strategy’s rules on each trade, assessed independently of the result. The process score separates two questions that most traders conflate: was this a good trade, and was this a well-executed trade? These are genuinely different questions, and conflating them produces exactly the kind of bias that makes review sessions useless.

A well-executed trade that lost money is not a bad trade. It is evidence about the system’s variance during that period. A poorly executed trade that made money is not a good trade. It is a warning that the positive outcome is masking a process failure that will eventually produce a loss at a moment when the stakes are higher. Keeping these two assessments separate allows the review to build an accurate picture of two distinct things: whether the strategy has genuine edge when executed correctly, and whether the trader is actually executing it correctly.

The process score should be simple enough to complete in under thirty seconds per trade. A four-criterion binary checklist — entry conditions fully met, stop at the correct structural level, correct position size, exit at the predetermined target or stop without discretionary modification — produces a score from zero to four. The rolling average of this score across the last twenty trades is one of the most informative numbers in the entire journal. A declining process score during a drawdown is almost always the first signal that the drawdown has a behavioral component rather than a purely statistical one.

“A losing trade that scores four out of four on process is information about variance. A winning trade that scores one out of four is a warning about something the positive outcome is temporarily hiding.”

PRACTICAL APPLICATION

Add a process score column to your trade log immediately. Score every trade from the last thirty days retroactively using the four-criterion checklist. Then calculate average R separately for trades that scored three or four versus trades that scored zero, one, or two. This single segmentation almost always reveals a material performance difference between clean executions and compromised ones — and it converts the abstract goal of “trade better” into a specific, measurable target: increase the percentage of trades that score three or four.

THE WEEKLY REVIEW: STRUCTURE AND SEQUENCE

The weekly review is the central analytical unit of an honest review process. Weekly is the correct cadence: long enough to contain a statistically meaningful sample of trades, short enough to catch problems while they are still correctable.

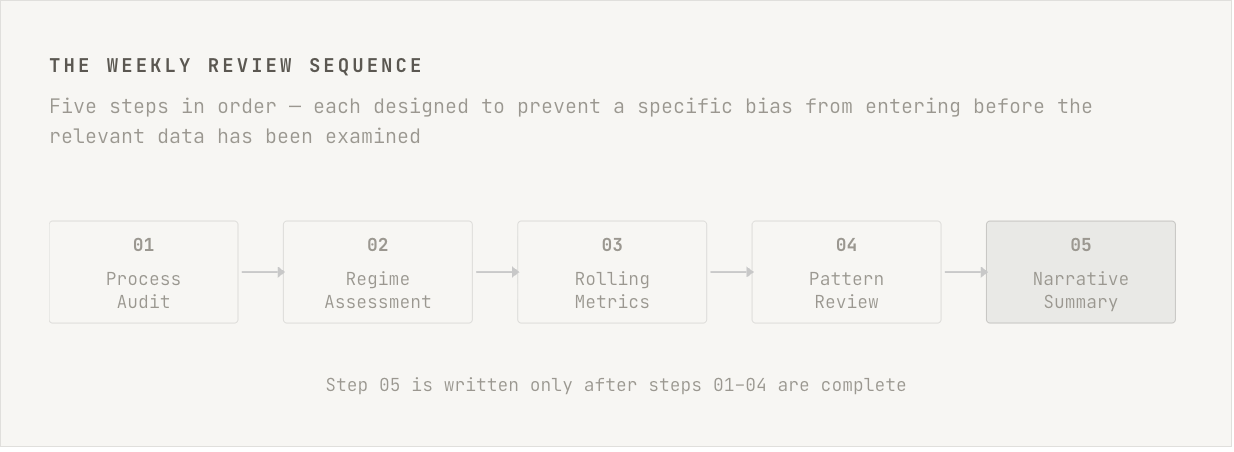

The weekly review must follow a specific sequence to remain honest. Each step is designed to prevent a specific form of bias from entering before the relevant data has been examined. The correct order is: process before outcomes, regime before results, rolling metrics before individual trades, and patterns before explanations. Deviating from this sequence — for example, starting by looking at the equity curve for the week — contaminates every subsequent assessment with the emotional frame that the equity curve creates.

Step one is the process audit. Review every trade taken during the week and score it on the four-criterion checklist. Calculate the week’s average process score. If it is below the rolling baseline, that is the first finding of the review and it should be documented before moving to anything else. Step two is the regime assessment. What were the market conditions during the week? Were they consistent with the environments in which the strategy’s historical parameters were established? Step three is the rolling metrics review: rolling twenty-five trade expectancy, rolling process score trend, and the current drawdown percentile within the Monte Carlo distribution. Step four is the pattern review: are there specific setup types, session times, or market conditions under which performance is systematically better or worse? Step five, only after the first four are complete, is the narrative summary — one paragraph describing what the week’s data shows, written in factual rather than evaluative language.

PRACTICAL APPLICATION

Set a fixed weekly review time — the same day, the same hour, every week — and treat it as non-negotiable as the trading session itself. The review should take between thirty and sixty minutes. Use a written template with the five steps listed in order and a space for each output. Complete them in sequence. Never write the narrative summary before completing the first four steps.

READING PATTERNS ACROSS LARGE SAMPLES

Individual trade review, even when structured and honest, has limited diagnostic value. The signal in any individual trade is too weak to support confident conclusions about the system’s behavior. Pattern recognition — the ability to see systematic tendencies that only become visible across fifty, one hundred, or two hundred trades — is where the review process generates its most actionable insights.

The most valuable patterns to track are those that segment performance by a variable that should theoretically matter to the strategy. Session time is one: does the strategy perform differently in the first hour of the session versus the middle of the day? Setup type is another: are there variations of the core setup that consistently outperform or underperform others? Market regime is a third: is the strategy’s expectancy stable across different volatility regimes, or does it vary in ways that suggest the edge is regime-dependent? Each of these segmentations requires enough trades in each category to be statistically meaningful — typically at least twenty to thirty per category before conclusions are reliable.

The most useful pattern that most traders never track is the performance of their own decision-making relative to the mechanical rules. A trader who occasionally takes setups that partially meet the criteria, or manages trades in ways that deviate from the written plan, has introduced a discretionary layer. The question is whether that layer adds or subtracts value. The only way to know is to tag every trade as either rules-compliant or rules-deviant, track average R for each category over a large sample, and compare them. Most traders who do this for the first time find that their discretionary modifications subtract value — which is simultaneously discouraging and clarifying.

50+

The minimum number of trades in any single category before performance segmentation produces conclusions reliable enough to act on.

PRACTICAL APPLICATION

Choose one segmentation variable that is theoretically relevant to your strategy — session time, setup variation, regime type, or rules compliance — and begin tagging every trade with its category value immediately. Commit to collecting at least fifty trades in each category before drawing any conclusions. At the fifty-trade threshold, calculate average R for each category and look for differences larger than 0.15R per trade. Differences of this magnitude, sustained across a large sample, are almost certainly structural rather than random.

THE PASSED-ON TRADE LOG: MAKING INVISIBLE DATA VISIBLE

Every trader makes two types of decisions during a session: the decision to take a trade, and the decision not to take one. Most trade journals record only the first type. The result is a dataset that is systematically incomplete and biased toward the trader’s actual behavior rather than toward the strategy’s defined criteria.

The passed-on trade log is a record of every situation during the session where the setup criteria were met but the trader chose not to enter. For each passed-on setup, the record should include the conditions that were present, the reason for passing, and — reviewed after the fact — what the outcome would have been if the trade had been taken. This last element is uncomfortable to track because it sometimes reveals that the trader’s passing decisions are adding negative value: the setups they skipped were ones they should have taken, and the judgment they exercised in skipping them cost more than the anxiety it avoided.

The passed-on trade log also reveals a subtler problem: trades that were passed on for reasons that have nothing to do with the setup criteria. A trader who passes on a valid setup because they already had a loss that day, or because they were distracted at the moment the trigger fired, is not exercising strategic discretion. They are allowing non-systematic factors to determine which setups reach execution — and these filters are invisible in the trade log, only visible in the passed-on trade record.

PRACTICAL APPLICATION

For the next four weeks, log every passed-on setup alongside every taken trade. At the end of four weeks, review the passed-on log and calculate what average R would have been if every setup that met the full criteria had been taken. Compare that to the average R of the trades actually taken. The comparison reveals two things: whether your passing decisions are adding or subtracting value, and what the real reason is that each setup was passed — because the written reason and the actual reason are often not the same.

CONVERTING REVIEW INTO CHANGED BEHAVIOR

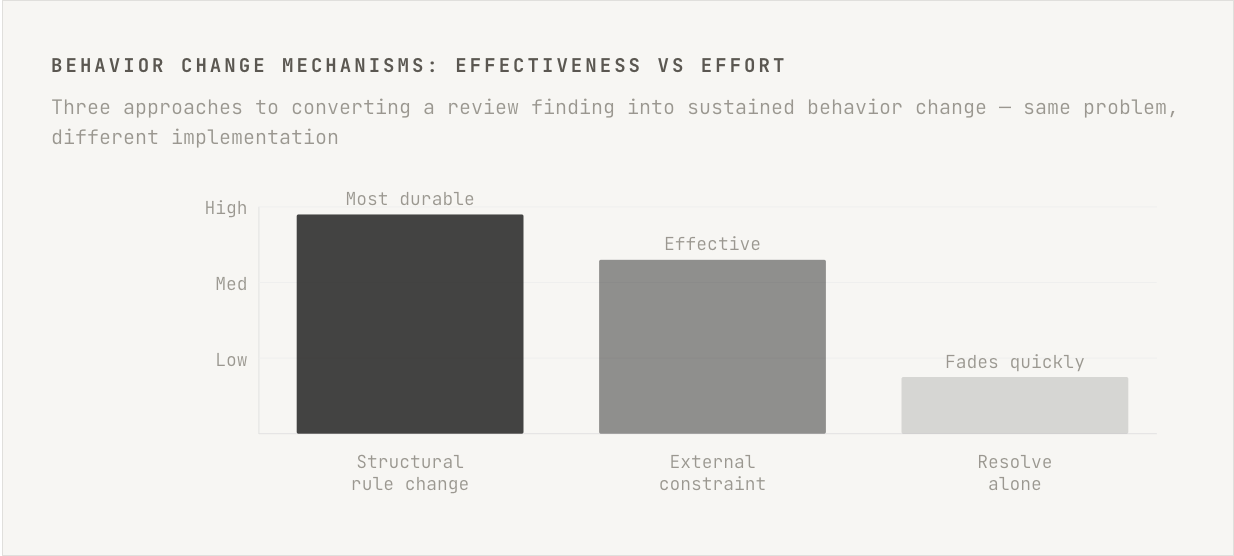

The most common failure of an otherwise well-structured review process is that the review produces accurate diagnoses and then nothing changes. The trader identifies that they are cutting winners short. They note it in the review. They resolve to stop doing it. The following week they cut winners short again. The resolve did not produce the behavior change because resolve without a mechanism is not a plan. It is a preference.

Behavior change in trading requires one of three things: a structural change to the rules that eliminates the problematic decision, an external constraint that prevents the problematic action from being taken, or a pre-committed protocol that specifies exactly what to do in the situation where the problematic behavior tends to occur. Of these three, the structural rule change is the most powerful because it removes the decision entirely. If cutting winners short is identified as a consistent problem, the structural solution is to define exit rules that do not require a decision at the moment of exit.

The external constraint approach works when structural changes are not possible. A trader who consistently over-sizes during winning streaks can implement a rule that position size must be calculated before the session and cannot be changed during it. A trader who revenge-trades after losses can implement a rule that no new trades are taken within a defined period after a stop is hit. The constraint does not require willpower in the moment because the decision was made in advance, at a time when emotional pressure was not present.

PRACTICAL APPLICATION

At the end of each weekly review, identify one specific behavior — not a general tendency — that the data shows is costing expectancy. Write it as precisely as you can: not “I cut winners too early” but “I am exiting winners before the target when the trade has been open for more than forty minutes and is showing a drawdown from peak.” Then write one structural change or external constraint that addresses this specific pattern. Implement only one change per review cycle. One precise change applied consistently produces more improvement than five simultaneous resolutions that all fade within a week.

THE MONTHLY AND QUARTERLY REVIEW: STRATEGIC ASSESSMENT

Weekly reviews address execution, process, and short-term behavioral patterns. Monthly and quarterly reviews address something different: whether the overall trading operation is developing in the direction it needs to go. These are strategic reviews rather than execution reviews, and they require a different analytical posture.

The monthly review should answer three questions. First, is the strategy’s expectancy trend moving in the right direction? Not the absolute level — which is dominated by variance at the monthly scale — but the trend over the last three to four months, smoothed through the rolling twenty-five trade metric. Second, is the process score trend improving, stable, or declining? Improving process scores with flat or negative expectancy is almost always a good sign — it suggests the execution is cleaning up and the statistical results will follow. Declining process scores with positive expectancy is a warning — luck is masking a behavioral problem that will eventually express itself in results. Third, is the behavior change implemented from the previous review cycle still in place?

The quarterly review adds a longer-horizon layer. It should include a regime analysis of the past quarter — what market environments were present, and how did the strategy’s performance map onto them? It should include a sample size assessment — are there enough trades in the review period to draw statistically reliable conclusions about the patterns being tracked? And it should include a forward look — given what the past quarter’s data shows, what is the one change to the strategy design, the position sizing, or the review process itself that would most improve expected performance over the next quarter?

PRACTICAL APPLICATION

Create a one-page monthly review template with exactly three sections: expectancy trend assessment, process score trend assessment, and behavior change follow-up. Complete it on the first weekend of each month using the previous month’s data. Keep every monthly review document. After six months, the collection of monthly reviews shows you whether the patterns you identified were real, whether the changes you implemented stuck, and whether the trajectory of your development is what you believed it was. The honest answer to that last question is often the most useful thing the review process produces.

CONCLUSION

The trade review is the mechanism through which a trader converts experience into information and information into improvement. Without it, experience accumulates but does not compound — the trader repeats the same errors because the errors are never clearly identified, and the same strengths go unexploited because their specific conditions are never precisely mapped. With a well-structured review, even a modestly talented trader with a genuine edge can achieve compounding improvement in execution quality that eventually exceeds what raw talent alone would produce.

The key word is structured. The natural human tendency in self-assessment — toward confirmation, toward narrative, toward remembering wins more vividly than losses, toward attributing success to skill and failure to circumstance — does not disappear because a trader decides to keep a journal. It disappears only when the review process is built with enough structural rules to prevent those tendencies from shaping the conclusions. Pre-entry recording before outcomes are known. Process scores evaluated independently of results. The weekly sequence completed in the correct order. Patterns identified across large samples. Behavior changes implemented as structural rules rather than intentions. Each of these is a specific defense against a specific form of bias.

The review process described in this newsletter is not comfortable. It reveals things about the trader’s actual behavior that a flattering self-assessment would conceal. It surfaces costs that outcome-focused review would attribute to bad luck. It forces an honest accounting of whether discretionary decisions are adding or subtracting value. None of that is pleasant. All of it is necessary for anyone who wants to develop a trading operation that improves systematically rather than oscillating between periods of false confidence and unnecessary self-doubt.

The journal does not lie. The trader does — to themselves, consistently, and in predictable directions. The structure of the review process is the only reliable defense against it.