How To Build Real Statistical Edge In Trading

A complete framework to create and apply statistics, so trading truly works.

This article is a deep, actionable guide to understanding what actually creates a real edge in trading.

It brings together the core principles of professional speculation: probabilistic thinking, expected value, structured setups, risk control, execution discipline, and the role of discretion.

It’s my hope that this framework helps traders stop treating markets like a prediction game and start approaching them like a repeatable statistical business.

With all that out of the way, let’s begin!

TRADING EDGE & PROBABILISTIC THINKING

Trading Is Not Prediction – Losing traders approach the market as if success comes from forecasting the outcome of the next move. Consistent traders think differently. They understand that markets are uncertain by nature and that no one can consistently predict the result of any single trade. A trading career is not built on isolated forecasts, but on whether a method produces positive results over a large sample. Focusing on prediction creates emotional pressure and short-term thinking; focusing on probability creates process, discipline and repeatability. Practical Application: Replace the question “Will this next trade win?” with “Does this setup make money over 100-500 repetitions?” That shift alone moves trading from guessing to system-building.

Think Like a Statistician, Not a Fortune Teller - A real trading edge is statistical. The goal is to find a pattern, setup or framework that produces favorable outcomes over time, even if many individual trades still lose. Once you stop demanding certainty from each trade, you stop overreacting to single outcomes. This reduces fear, revenge trading, and the need to be right. Practical Application: Judge your strategy by distributions, not anecdotes. One big win proves nothing. One bad loss proves nothing. What matters is the behavior of the system over many trades.

A Single Trade Means Very Little - One of the defining traits of professional traders is their ability to emotionally detach from individual outcomes. A single trade is just one data point inside a much larger sample. Emotional decision-making usually comes from over-weighting recent outcomes. If one win makes you euphoric or one loss makes you doubt the system, you are thinking too narrowly. Practical Application: Track performance in blocks of trades rather than trade-by-trade. Many traders benefit from reviewing results every 20, 50 or 100 trades instead of reacting after each position closes.

Edge Exists Only Across Repetition - A setup is not an edge simply because it worked a few times. It becomes an edge only if it can be repeated under clear conditions and still produce positive expectancy over time. Randomness can make weak systems look strong in the short run and strong systems look weak in the short run. Repetition is what separates luck from structure. Practical Application: Before increasing size or trusting a method, ask whether the setup has been observed, documented, and measured enough times to justify confidence.

EXPECTED VALUE & THE MATHEMATICS OF PROFITABILITY

Expected Value Is the Core of Every Trading Edge – At the center of professional trading sits a simple principle: expected value. Expected value measures how much a strategy is expected to make or lose on average per trade over time. Why It Matters: Without positive expected value, no amount of confidence, chart reading, or effort will save a strategy in the long run. If expectancy is negative, repetition only magnifies losses. Practical Application: Evaluate every strategy through the lens of expectancy, not just raw win rate.

The Formula That Matters – Expected value can be expressed as:

𝐸 = (𝑃𝑤𝑊)-(𝑃𝑙𝐿)

Here, 𝑃𝑤 is the probability of winning, 𝑊 is the average win, 𝑃𝑙 is the probability of losing and 𝐿 is the average loss. This formula makes something very clear: profitability is a combination of frequency and magnitude. You do not need to win often if your wins are much larger than your losses. Practical Application: Instead of obsessing over being “right,” focus on improving one of the core drivers of expectancy: win rate, average win or average loss.

Win Rate Alone Is Misleading – Many traders incorrectly assume that a high win rate is the same thing as a good strategy. It is not. A strategy can win often and still lose money if its losses are too large, while another can win less than half the time and still be highly profitable if its winners are large enough. This misconception traps traders in low-quality systems that feel good psychologically but perform poorly mathematically. Practical Application: Always pair win rate with risk-reward. A 45% win rate with 3R winners can be stronger than a 70% win rate with poor loss control.

Large Wins Can Outweigh Frequent Losses - Imagine a system that wins only 45% of the time, but each winner averages three times the size of each loser. Such a system can still produce strong positive expectancy. Why It Matters: This is one of the most important lessons in trading: you do not need to be right most of the time to make money. You need the value of wins to exceed the value of losses over a large enough sample. Practical Application: When reviewing your journal, don’t just count wins and losses. Measure average R on winners, average R on losers, and the total expectancy of the system.

MARKET HYPOTHESIS & WHY A STRATEGY SHOULD WORK

Every Edge Begins With a Market Hypothesis – Before a trader can build a real system, they need an explanation for why the setup should work. This is called a market hypothesis. It is the underlying logic behind the strategy. Without a hypothesis, a setup is just pattern memorization. A trader may execute it mechanically for a while, but they won’t understand when conditions support it or when they do not. Practical Application: For every setup you trade, be able to answer this question clearly: “What market behavior am I trying to exploit?”

Markets Reflect Repeating Participant Behavior – Financial markets are shaped by institutions, hedge funds, retail traders, algorithms and liquidity-seeking behavior. Although markets are uncertain, participants often behave in recurring ways and those behaviors create temporary inefficiencies. A strategy becomes stronger when it is tied to behavior rather than just shape. Patterns matter less than the participant logic underneath them. Practical Application: Study the incentives behind price movement. Ask what traders, funds or liquidity providers are likely doing around your setup.

Trend Persistence Is One Common Source of Edge - One recurring market behavior is momentum continuation. When strong directional movement begins, price often keeps moving further than many expect. This supports trend-following or momentum-based systems. Trends persist because participants adjust gradually, not instantly. Flows, positioning and herding can extend directional moves. Practical Application: If you trade momentum, define how you identify a genuine expansion phase and how you distinguish it from noise.

Liquidity Behavior Creates Another Source of Edge - Retail traders often cluster stop losses around obvious highs, lows and clean technical levels. Larger players are aware of this and price may sweep those zones before reversing. Liquidity is not random; it tends to accumulate where human behavior is predictable. This creates opportunities for traders who understand stop placement and order-flow dynamics. Practical Application: Build setups around liquidity maps, failed breakouts or stop-sweeps only if you can define those conditions precisely and test them consistently.

Mean Reversion Is Another Repeatable Dynamic – Markets sometimes stretch too far away from equilibrium due to panic, greed or temporary imbalance. When they do, price often reverts toward a more normal range. This creates opportunity for traders who can identify overextension rather than chasing it. Practical Application: If you trade mean reversion, define what “too far” means in measurable terms, such as distance from moving averages, volatility bands or session range expansion.

SETUP DESIGN & RULE-BASED EXECUTION

A Setup Must Be Precise to Be Testable - Many traders describe their approach in vague terms like “buy support” or “sell weakness.” Those phrases sound sensible but are too loose to test properly. If your rules are ambiguous, your results are meaningless because you are not repeating the same process each time. Practical Application: Define entry criteria, stop placement, context filters and exit rules with enough precision that another trader could understand and replicate them.

Repeatability Creates Reliable Data - A strategy only becomes measurable when the same setup occurs over and over under the same rules. Without repeatability, there is no valid sample. Without a valid sample, there is no way to know whether the strategy actually has an edge. Practical Application: Write your setup like a checklist. Include market condition, higher-timeframe context, entry trigger, invalidation point and management rules.

Context and Trigger Should Be Separate - A strong trading model usually has two layers: context and trigger. Context defines the broader environment in which the trade makes sense. Trigger defines the specific condition that causes entry. Many traders confuse the two. They either trade a signal with no broader logic, or they have a good bias but no precise execution mechanism. Practical Application: For example, your context might be “higher-timeframe uptrend with pullback into value,” while your trigger might be “lower-timeframe momentum expansion off that zone.”

Vague Rules Create Inconsistent Psychology - Ambiguous setups do not just hurt testing; they also damage decision quality in real time. If rules are unclear, fear and greed will fill the gaps. Emotional trading often begins where structural clarity ends. Practical Application: Whenever you notice indecision during live execution, review whether the setup itself is too loosely defined.

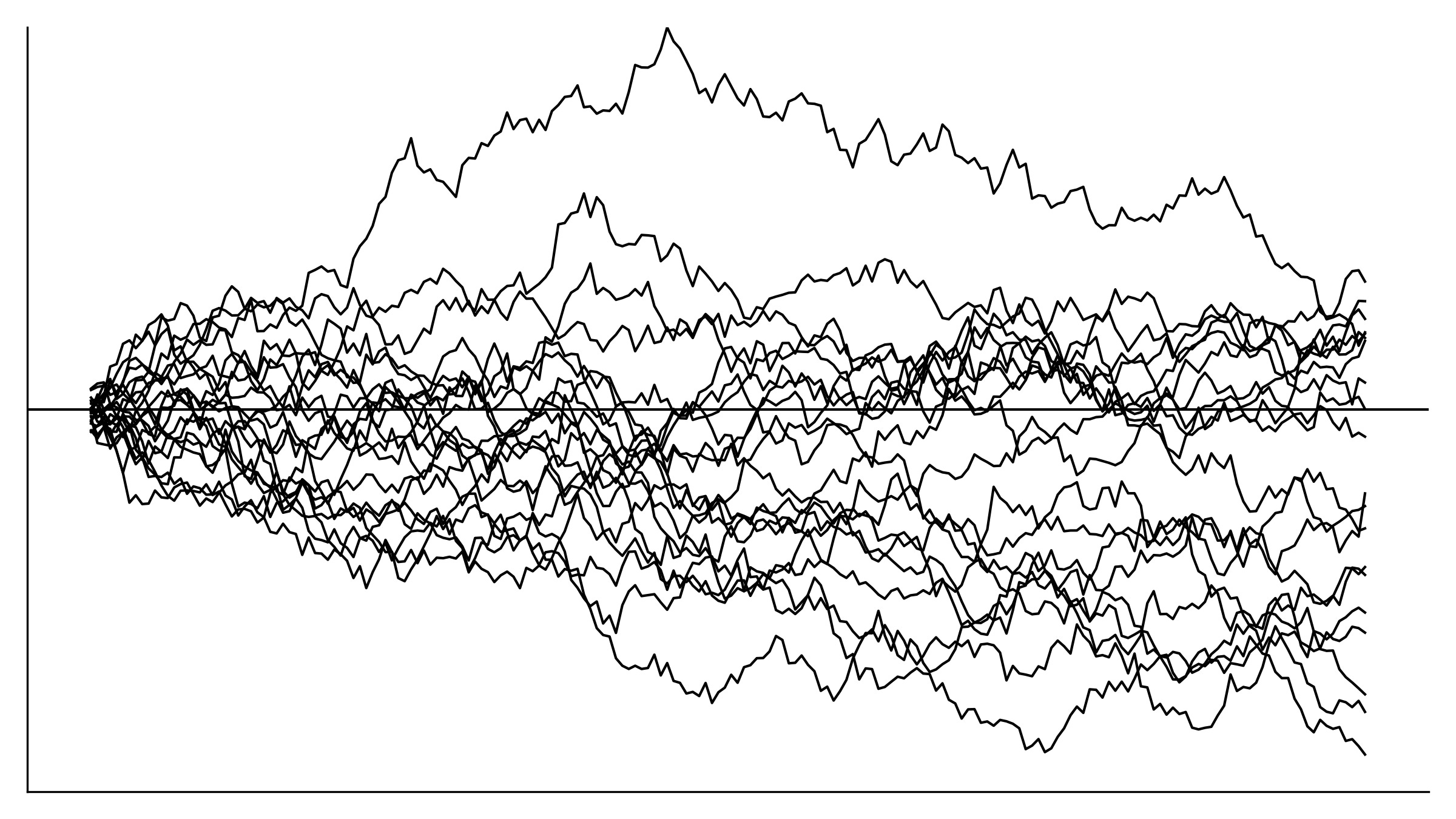

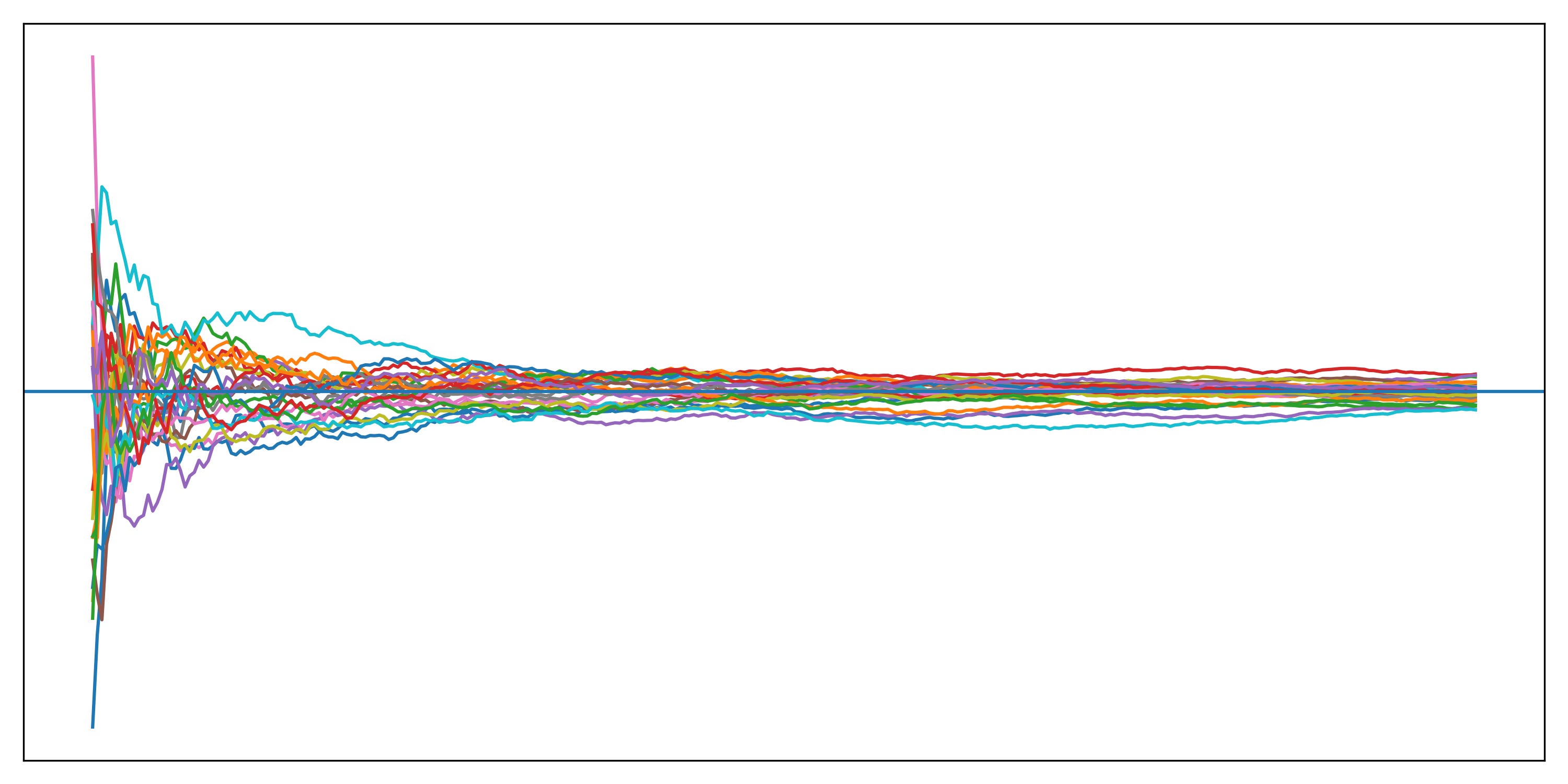

SAMPLE SIZE, RANDOMNESS & STATISTICAL VALIDITY

Small Samples Are Deceptive - One of the most common mistakes among developing traders is judging a system after only a few trades. A handful of wins can create false confidence, while a handful of losses can cause a solid strategy to be abandoned prematurely. Small samples are dominated by noise. Randomness can easily distort short-term outcomes. Practical Application: Resist the urge to conclude too early. A strategy should usually be judged over dozens, and preferably hundreds, of comparable trades.

Randomness Can Make Bad Systems Look Good - Ten wins in a row may feel like proof, but it may simply be variance. A weak strategy can look excellent for a while if randomness is favorable. Traders often mistake lucky runs for edge, then scale up into eventual failure. Practical Application: Treat hot streaks with skepticism unless they are supported by meaningful sample size and stable execution quality.

Randomness Can Also Hide Good Systems - The reverse is also true. A profitable system can begin with several losses or a poor opening month. That does not automatically invalidate it. Traders who lack statistical patience often quit systems right before the edge would begin to reveal itself. Practical Application: Compare actual performance not just to recent outcomes, but to the expected drawdown and losing streak profile of the system.

Large Samples Reveal the Truth - As the number of trades increases, the underlying structure of the strategy becomes easier to see. Randomness never disappears completely, but its distortions weaken over time. This is why professionals often evaluate systems only after a substantial trade count. Large samples provide a more honest picture of expectancy, variance and execution consistency. Practical Application: Maintain clean records and review your edge across large enough datasets to separate luck from structure.

OPTIMIZING EXPECTANCY & IMPROVING THE SYSTEM

Entry Efficiency Improves Risk-Reward - Once a strategy has positive expectancy, one of the first areas to improve is entry quality. Better entries reduce risk relative to potential reward. If you can enter closer to invalidation without hurting win rate too much, expectancy improves immediately. Practical Application: Review your entries and ask whether timing or confirmation can be refined to reduce risk and improve R multiple potential.

Exit Structure Strongly Shapes Average Win - Many traders have decent entries but poor exits. They cut winners too early, especially after a few recent losses or when unrealized profit creates anxiety. Premature exits cap the upside of the strategy and often destroy the payoff profile that gives the system its edge. Practical Application: Review whether your exits are aligned with the logic of the setup, or whether they are being dictated by emotion.

Loss Containment Protects Expectancy - Average loss is just as important as average win. Even a good strategy can be ruined if losing trades are allowed to expand unpredictably. One oversized loss can erase the gains from many well-executed trades. Practical Application: Keep invalidation rules strict. If the trade is wrong, accept it and move on. Expectancy is protected through controlled downside.

Optimization Should Improve Structure, Not Distort It - Traders often damage promising strategies by over-optimizing around recent data. Small tweaks can help, but endless adjustment can turn a robust idea into curve-fit noise. Improvement is useful only when it preserves the core logic of the edge. Practical Application: When optimizing, focus on durable improvements such as cleaner entries, clearer filters and better risk control rather than constantly redesigning the system after every drawdown.

POSITION SIZING & RISK MANAGEMENT

A Strong Edge Can Still Fail With Bad Risk Management – Even a profitable strategy can blow up if position sizing is reckless. The quality of the system and the quality of risk management are separate issues. Edge determines whether the game is worth playing; risk management determines whether you survive long enough to let that edge play out. Practical Application: Never assume good setups justify oversized risk. Survival comes first.

Risk Small, Risk Consistently - Professional traders usually risk a small, repeatable percentage of capital on each trade rather than swinging heavily between positions. Consistency in risk allows the strategy’s statistical profile to emerge cleanly. Inconsistent sizing distorts results and increases emotional pressure. Practical Application: Choose a fixed risk model that keeps drawdowns manageable and allows you to execute without panic.

Losing Streaks Are Normal - Even profitable systems experience sequences of losses. This is not a sign of failure; it is part of the distribution. Traders who size too aggressively cannot psychologically or financially survive normal losing streaks. Practical Application: Estimate the likely losing streak profile of your system and make sure your risk model can withstand it comfortably.

Survival Is a Core Trading Skill - Trading is not about maximizing one trade, one day, or one week. It is about staying in the game long enough for compounding and expectancy to matter. Accounts are not usually destroyed by lack of opportunity, but by lack of survival discipline. Practical Application: Build your process so that a bad week or bad month cannot remove you from the game.

EXECUTION CONSISTENCY & PROCESS DISCIPLINE

A Strategy Only Works If You Actually Follow It - Traders spend enormous energy searching for better systems while ignoring the bigger issue: inconsistent execution. Even a profitable system fails when it is applied selectively and emotionally. Once rules are broken, results no longer reflect the system. They reflect a mixture of the system plus random emotional interference. Practical Application: Separate strategy review from execution review. Ask not only “Is the system good?” but also “Did I actually trade it as written?”

Stress Causes Rule-Breaking - Traders often skip valid trades after a recent loss, widen stops to avoid being wrong or take profits too early out of fear. These behaviors are understandable, but they corrupt the statistical structure of the edge. Once execution becomes inconsistent, expectancy becomes unknowable. Practical Application: Journal not just trade outcomes, but rule adherence. A losing trade taken correctly is still a good trade. A winning trade taken incorrectly is still a process failure.

Discipline Makes Results Measurable - Professionals aim to execute their systems with near-algorithmic consistency. They know that only disciplined repetition produces reliable data and long-term confidence. Confidence should come from evidence and repetition. Practical Application: Reduce unnecessary improvisation. Use checklists, pre-trade routines, post-trade review and clear invalidation rules to minimize impulsive behavior.

JOURNALING, FEEDBACK & CONTINUOUS IMPROVEMENT

A Trading Journal Turns Experience Into Data - Traders who do not record their trades are effectively wasting information. Every trade contains lessons about the system, the market, and the trader’s own behavior. Without records, memory becomes selective and biased. A journal creates objective feedback. Practical Application: Track entries, exits, stop location, context, market condition, result in R, and whether the trade followed the plan.

Reviewing Trades Reveals Hidden Patterns - Over time, a journal can show which setups work best, which market environments reduce performance, and which mistakes recur most often. Improvement becomes possible only when problems are visible. Practical Application: Periodically review your data by setup type, session, volatility regime and execution quality to see where performance is strongest or weakest.

Trading Becomes a System When It Is Measured - The act of tracking, reviewing and refining moves trading away from intuition-only behavior and toward a process that can actually be improved. Serious traders do not just “have opinions.” They gather evidence. Practical Application: Treat your journal like a research tool, not a diary. The goal is to generate usable insight, not just record emotions.

DISCRETION & THE ADVANCED LAYER OF TRADING

Mechanical Rules Come First - Discretion is valuable, but only after a trader has already built a tested statistical foundation. Before that point, “discretion” often just means emotional inconsistency. Without structure, intuition is unreliable and impossible to evaluate. Practical Application: Earn the right to use discretion by first proving that you can define, test and execute a system consistently.

Discretion Is Contextual Judgment, Not Randomness - True discretion means interpreting market conditions and deciding whether the current environment supports the underlying logic of the strategy. It is not abandoning the system on impulse. Markets are dynamic. Two setups may look similar on the chart while taking place in very different volatility, liquidity or macro conditions. Practical Application: Use discretion to ask whether the environment still matches the type of market your system is built for.

Market Regimes Matter - A setup that performs well in stable, orderly conditions may perform poorly during highly volatile, news-driven or liquidity-distorted periods. Experienced traders often reduce size, filter trades, or stand aside in those environments. Context can change the quality of the same visible pattern. Practical Application: Build regime awareness into your process by noting volatility conditions, scheduled news risk, and broader macro context around your setups.

Discretion Can Improve Trade Management - Even when entries and exits are rule-based, experienced traders sometimes adapt management based on evolving conditions. Strong momentum may justify allowing a winner to run longer, while sudden weakness may justify reducing exposure sooner. Real markets are more fluid than static backtests. Practical Application: If you use discretionary management, document it carefully so that it remains a skill to refine rather than an excuse for inconsistency.

Discretion Must Be Built on Observation - Genuine discretion develops through hundreds or thousands of observed trades. It is the result of pattern recognition grounded in experience, not confidence alone. Many traders try to start with advanced judgment before earning it. That usually leads to inconsistency disguised as sophistication. Practical Application: Treat discretion as an advanced layer added only after the baseline system is already statistically sound.

THE BALANCED MODEL: STRUCTURE + JUDGMENT

The Best Traders Combine System and Adaptation - Pure mechanical structure provides measurement, consistency and a statistical foundation. Thoughtful discretion adds contextual awareness and flexibility. Trading is too dynamic for blind rigidity, but too unforgiving for unstructured intuition. The strongest approach combines both. Practical Application: Build a repeatable core system first, then gradually layer in discretionary refinements that can be documented, reviewed and validated.

Statistical Discipline Comes First, Human Judgment Comes Second – The proper order matters. Traders should first master rule-based execution, risk management and expectancy. Only then should they expand into nuanced adaptation. When the order is reversed, discretion becomes chaos. When the order is correct, discretion becomes enhancement. Practical Application: Ask yourself whether your “adaptation” improves the system measurably or simply changes it emotionally from day to day.

Trading Is a Probability Business - In the end, professional trading is about building a system where probabilities work in your favor, executing that system consistently, managing risk intelligently and allowing the edge to unfold over time. This is the mindset that separates amateurs from professionals. Practical Application: Stop trying to know what the market will do next. Focus on creating a process that remains profitable even when you do not.

Finally, the deepest shift in trading happens when a trader stops asking how to predict the next move and starts asking how to build a repeatable edge. That transition changes everything. It changes how setups are designed, how trades are judged, how losses are handled and how progress is measured. The market will always remain uncertain, but a trader does not need certainty to succeed. What they need is a positive expectancy, execution, sound risk control and enough patience to let the numbers work in their favor. When structure and judgment are combined properly, trading stops being a guessing game and becomes what it truly is at the professional level - a long-term process of probabilistic decision-making under uncertainty.

Absolutely incredible article bro. This is the reality of trading