How to Build a Watchlist That Actually Works

Most traders treat the watchlist as a collection of names they are interested in. Professional traders treat it as the output of a structured filtering process that narrows the entire market down to the specific situations where their edge has the highest probability of being present. Those are not the same thing.

The distinction matters more than it initially appears. A watchlist built from general interest, recent news flow, or social media attention produces a list of tickers with varying degrees of relevance to the trader’s actual setup criteria. Some will be genuinely actionable. Most will not. The trader spends the session monitoring a mixture of real opportunities and noise, unable to clearly separate the two until after the session is over and the opportunity has already passed.

A watchlist built from a structured filtering process arrives at the session ready. Every name on it has already passed through a sequence of criteria that align with the trader’s specific edge. The setup conditions are partially or fully in place. The scenarios are written down in advance. When the market opens and begins moving, the trader is not deciding what to watch. They are executing a prepared plan against a predetermined set of situations.

This newsletter is about how to build the second kind of watchlist. The filtering logic, the scenario construction, the regime awareness, the sizing of the list, and the discipline required to stay within it during the session are all components of a process that most traders have never formalized and most profitable traders have never abandoned.

[Download the full printable PDF below.]

THE WATCHLIST IS NOT A UNIVERSE, IT IS A FILTER OUTPUT

The starting point for understanding how a professional watchlist works is recognizing what it is not. It is not a list of things worth watching. Virtually anything in a liquid market is worth watching under the right conditions. The watchlist is the output of a filtering process that applies the trader’s edge criteria to the available universe of instruments and returns only the situations where those criteria are met or nearly met. Everything else, regardless of how interesting or newsworthy, does not belong on it.

This requires having edge criteria that are specific enough to function as a filter. A trader whose setup is “strong momentum in the direction of the higher timeframe trend with a pullback into value” can apply that criterion systematically to a defined universe and produce a list of candidates that meet it. A trader whose approach is “stocks that look strong” cannot build a watchlist in any meaningful sense because the criterion has no filtering power. The quality of the watchlist is bounded by the precision of the underlying strategy.

The universe itself also requires definition. Professional traders in equities typically scan a defined universe of liquid names rather than the entire market, because the entire market contains too many low-quality setups to filter efficiently. In futures and forex, the universe is smaller by nature but still benefits from pre-session filtering. The universe definition is the first layer of the filter. The setup criteria are the second. The scenario construction, which this newsletter addresses in detail, is the third. Each layer reduces the list further. The goal is not comprehensiveness. It is precision.

PRACTICAL APPLICATION

Define your universe before defining your watchlist process. Write down the specific instruments or categories of instruments that are eligible to appear on your watchlist and the reason each is eligible. In equities, this might be a list of the most liquid names in specific sectors with average daily volume above a defined threshold. In futures, it might be the specific contracts your strategy is designed for. The universe definition is a standing filter that rarely changes. The watchlist is what that universe produces each session when your setup criteria are applied to it.

THE STRUCTURAL FILTER: HIGHER TIMEFRAME FIRST

The first substantive filter in any well-constructed watchlist process is the higher timeframe structure. Before a name can be considered for the session watchlist, the higher timeframe context should support the underlying logic of the setup. This is the context layer of the two-layer setup model applied at the pre-session stage rather than at the moment of entry.

For a trader who works primarily on intraday timeframes, the higher timeframe filter typically operates on the daily or weekly chart. The question being asked is whether the broader structural picture is aligned with the type of trade the strategy is designed to take. A momentum continuation strategy applied to names that are in clearly defined daily uptrends, above key moving averages, and showing expanding rather than contracting range will produce a different quality of opportunity than the same strategy applied indiscriminately to everything that moved yesterday.

The structural filter eliminates a significant portion of the initial universe before any session-specific analysis is conducted. Names that are in structurally unfavorable positions for the strategy, regardless of any intraday signal that might appear, are removed from consideration before the session begins. This prevents the trader from being drawn into a technically valid intraday signal that exists within a higher timeframe context that opposes it, which is one of the most reliable ways to generate a win rate that looks good on paper and performs poorly in practice.

“The higher timeframe filter is not about finding the best setups. It is about eliminating the ones where the underlying logic of the strategy is structurally opposed before the session even opens.”

PRACTICAL APPLICATION

Define two or three specific higher timeframe criteria that must be present for a name to pass the structural filter and become eligible for the session watchlist. Write these criteria as observable, measurable conditions rather than general descriptions. Apply them to your defined universe each evening as the first step in the pre-session process. The names that pass this filter become the pool from which the session watchlist is drawn. The names that do not pass are excluded regardless of any other characteristics they might have.

THE CATALYST FILTER: WHY IS THIS NAME MOVING?

After the structural filter, the second substantive question is whether there is a reason for the instrument to behave differently in the upcoming session than it has in recent sessions. This is the catalyst filter, and it operates differently depending on the trader’s strategy and market.

In equities, catalysts are often discrete and identifiable. An earnings release, a guidance revision, a sector rotation, a significant news event, a technical breakout on elevated volume — each of these creates a specific behavioral dynamic that may or may not align with the strategy. A momentum trader who exploits the continuation of strong directional moves will benefit from the presence of a genuine catalyst that creates durable participant interest rather than a single-session spike that reverses. A mean reversion trader will be interested in the post-catalyst overreaction dynamic rather than the initial move itself.

In futures and forex, catalysts are often scheduled — central bank decisions, employment data, CPI prints, geopolitical developments — and the catalyst filter operates more as a risk awareness layer than a selection layer. The relevant question for a session watchlist in these markets is not just “what might move this” but “what scheduled events create risk conditions that either support or oppose my setup criteria during this specific session?” A setup that performs well in clean, uninterrupted directional conditions may not belong on a watchlist for a session that contains a major data release at a key time.

PRACTICAL APPLICATION

Build a two-part catalyst review into your pre-session process. First, identify any scheduled events during the upcoming session that affect any name currently passing your structural filter, and assess whether those events support or oppose your setup criteria. Names where a scheduled event creates conditions that oppose the setup should either be removed from the watchlist or flagged with a specific note about the risk. Second, identify any recent unscheduled catalysts — earnings, news, volume spikes — and assess whether the resulting behavioral dynamic aligns with what your strategy is designed to exploit. Document the catalyst assessment for each name so that the watchlist contains not just the names but the reason each belongs there.

THE SCENARIO: CONVERTING A NAME INTO A TRADE IDEA

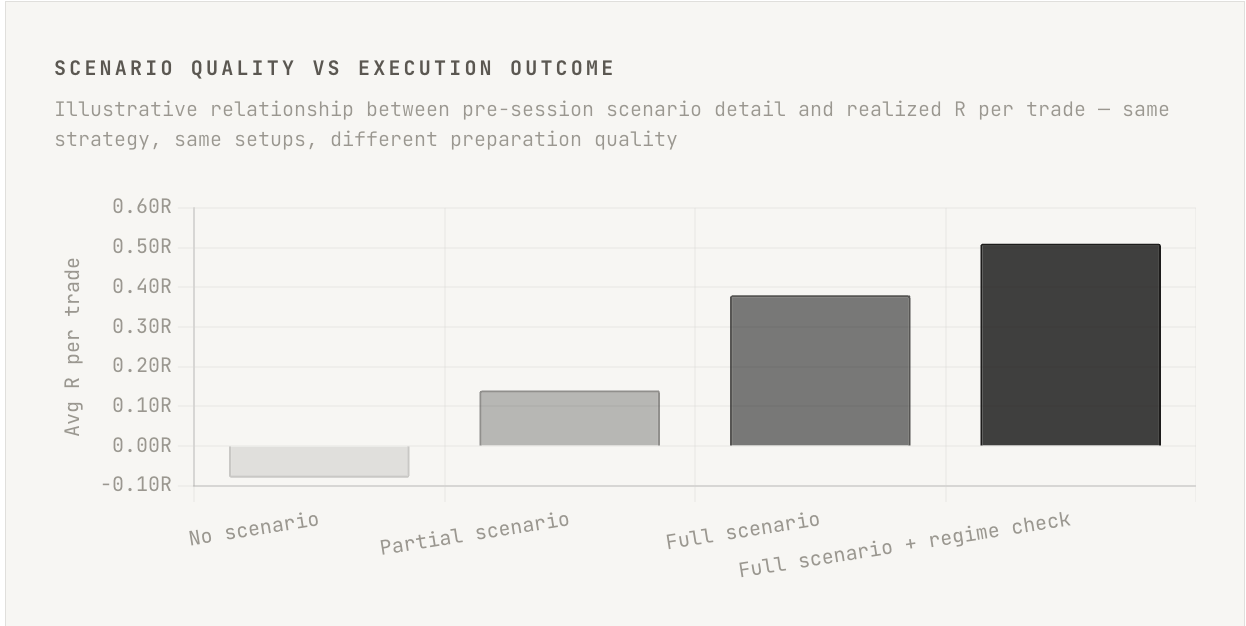

A name that passes the structural filter and the catalyst filter is a candidate, not a trade idea. The conversion from candidate to trade idea happens through scenario construction. A scenario is a written description of the specific conditions under which the trader will take action — what the market needs to do, at what level, in what sequence — before the entry trigger is reached. Without a scenario, the name on the watchlist produces reactive trading. With a scenario, it produces prepared trading. The difference in execution quality between those two modes is substantial.

A well-constructed scenario has three components. The first is the level or zone where the setup becomes relevant. This is not a precise price point but a defined area where the trader’s entry criteria are likely to be met if the market reaches it. The second is the condition that needs to be present when the market reaches that level — the lower timeframe confirmation, the volume behavior, the momentum character. The third is the invalidation, defined in advance, that tells the trader the scenario has not played out as anticipated and no trade should be taken.

The scenario construction process is where most of the analytical work happens, and it happens before the session rather than during it. A trader who has constructed clear scenarios for five names enters the session knowing exactly what they are looking for on each. A trader who has not constructed scenarios enters the session with five names and no plan, which means every piece of price action on those names requires a fresh analytical decision under real-time conditions. The quality of analytical decisions made in real time under emotional conditions is reliably lower than the quality of decisions made in advance during calm preparation.

PRACTICAL APPLICATION

For each name on the session watchlist, write a scenario that completes the following structure: “If price reaches [level or zone], and [lower timeframe condition is present], then I will [specific entry action] with a stop at [invalidation level] and a target at [logical exit level]. This trade is invalidated if [specific condition occurs].” The scenario should be specific enough that another trader with your strategy rules could read it and take the same trade at the same time. If it is not that specific, it is not yet a scenario. It is a general bias, and general biases produce inconsistent execution.

REGIME AWARENESS: MATCHING THE LIST TO THE DAY

Not every session is appropriate for every type of setup. Market regimes change across sessions as well as across longer periods, and a watchlist that does not account for the expected session character will consistently include names where the setup logic is not supported by the day’s likely behavior. This is regime awareness applied at the session level rather than the strategic level.

Session regime assessment asks a specific set of questions before the watchlist is finalized. Is this a session with significant scheduled news risk that is likely to produce choppy, reactive price action rather than clean directional movement? Is the broader market in a state of elevated volatility that tends to produce false breakouts and stop hunts rather than sustained momentum? Is liquidity likely to be reduced due to time-of-year factors or market holiday proximity? Each of these conditions changes the quality of certain types of setups in predictable ways, and the watchlist should reflect those changes rather than being built as if every session is identical.

A momentum trader building a watchlist for a session that contains a Federal Reserve announcement at a key time should either exclude momentum continuation setups from the watchlist entirely for that session, restrict the list to names that are unlikely to be directly affected by the announcement, or flag every name with a specific note about how the announcement changes the scenario. Ignoring the session regime and building the same watchlist regardless of what the day looks like produces a list that is only partially relevant to the actual opportunities the session will contain.

3-5

The optimal number of names on a session watchlist. More than five and attention is too diluted for high-quality execution. Fewer than three and the sample is too small to produce a trade.

PRACTICAL APPLICATION

Add a session regime assessment as the final step before the watchlist is finalized each evening. Rate the upcoming session on two dimensions: directional clarity, meaning how likely the session is to produce the type of clean movement your strategy requires, and event risk, meaning how likely scheduled or anticipated events are to disrupt the setups on the list. If both dimensions are unfavorable, reduce the watchlist to your highest-conviction candidates only and reduce intended position sizes accordingly. If both are favorable, execute the full watchlist at normal parameters. The assessment should take no more than five minutes and should be documented alongside the watchlist.

LIST SIZE: WHY FEWER NAMES PRODUCE BETTER RESULTS

One of the most counterintuitive findings in trading process analysis is that smaller watchlists tend to produce better execution quality than larger ones. The instinct is to build a comprehensive list because more opportunities seem better. The reality is that each additional name on the list beyond a certain threshold dilutes the quality of attention the trader can give to any individual name, increases the cognitive load during the session, and creates a larger surface area for impulsive decisions driven by whatever happens to be moving most visibly at any given moment.

The optimal watchlist size is constrained by the trader’s genuine capacity for simultaneous monitoring and execution. For most discretionary traders operating alone, that number is somewhere between three and six names. At three to six names, the trader can maintain genuine awareness of each name’s position relative to its scenario levels, respond appropriately when a setup triggers, and manage an open position while continuing to monitor the remaining candidates. Beyond six, something begins to get neglected. At ten or fifteen names, the watchlist has effectively become a market scanner output rather than a preparation document, and the trading that follows it will have the same reactive quality as market scanner-driven trading.

The discipline of keeping the list short also enforces the quality of the filtering process itself. A trader who is committed to a maximum of five names per session cannot afford to be vague in the structural or catalyst filters, because there is no room on the list for names that are merely interesting. Every slot has to be earned by a name that genuinely passes all the criteria. This constraint, experienced as a limitation, functions as a quality control mechanism that improves the list’s content without any additional analytical effort.

PRACTICAL APPLICATION

Set a hard maximum for your session watchlist and enforce it strictly. If the filtering process produces more candidates than the maximum, rank them by conviction — specifically by how cleanly each passes the structural and catalyst filters and how clearly the scenario is defined — and take only the top names. The ranking process itself is valuable because it forces an explicit quality comparison between candidates that the filtering process alone does not produce. Track your results separately for trades taken from the top of the conviction ranking versus trades taken from the bottom, and review whether maintaining the hard maximum improves overall expectancy over time.

THE PRE-SESSION REVIEW: MAKING THE LIST USABLE

A watchlist that is built the evening before and reviewed once before the session opens is more effective than one built in real time. A watchlist that is reviewed systematically as part of a pre-session routine is more effective still. The pre-session review is the process of converting the document from something the trader created into something the trader knows — the difference between having a plan and being ready to execute it.

The pre-session review should cover each name on the list in sequence, refreshing the trader’s mental model of the scenario for each. What is the level or zone where the setup becomes relevant? What is the condition that needs to be present? What is the invalidation? If the overnight session has moved any name significantly, the scenario may need to be updated before the regular session opens. If a name has already moved through its scenario level while the trader was not monitoring, it should be removed or the scenario rebuilt for the new price structure.

The review also serves a psychological function. A trader who has walked through each name’s scenario in detail before the session opens is operating from memory rather than from analysis during the session itself. When a name approaches a scenario level, the trader already knows what they are looking for rather than having to reconstruct the analysis under time pressure. That shift from real-time analysis to real-time execution of a prepared plan is one of the most significant improvements available to a trader who has not yet formalized a pre-session review process.

PRACTICAL APPLICATION

Build a fifteen to twenty minute pre-session review into your routine at a fixed time before the market opens. Work through each name on the watchlist in sequence. For each name, verbalize or write the scenario in your own words as if explaining it to another trader. Check whether overnight price action has changed the structure in a way that invalidates or modifies the scenario. Confirm that the risk parameters — position size, stop level, target — are still appropriate given the current price. Any name that you cannot walk through clearly in under two minutes during the review probably does not have a well-defined scenario, and that problem is better resolved before the session than during it.

SESSION DISCIPLINE: STAYING WITHIN THE LIST

The watchlist built before the session is only valuable if the trader uses it during the session. This sounds obvious but in practice it is one of the most consistently broken disciplines in active trading. The session will produce movement in names that are not on the watchlist. Some of those movements will look like excellent setups from a visual perspective. The filter criteria that excluded those names from the watchlist — the higher timeframe structure, the catalyst assessment, the regime alignment — are not visible in the moment of an exciting intraday move. What is visible is the move itself, and the move generates the impulse to participate.

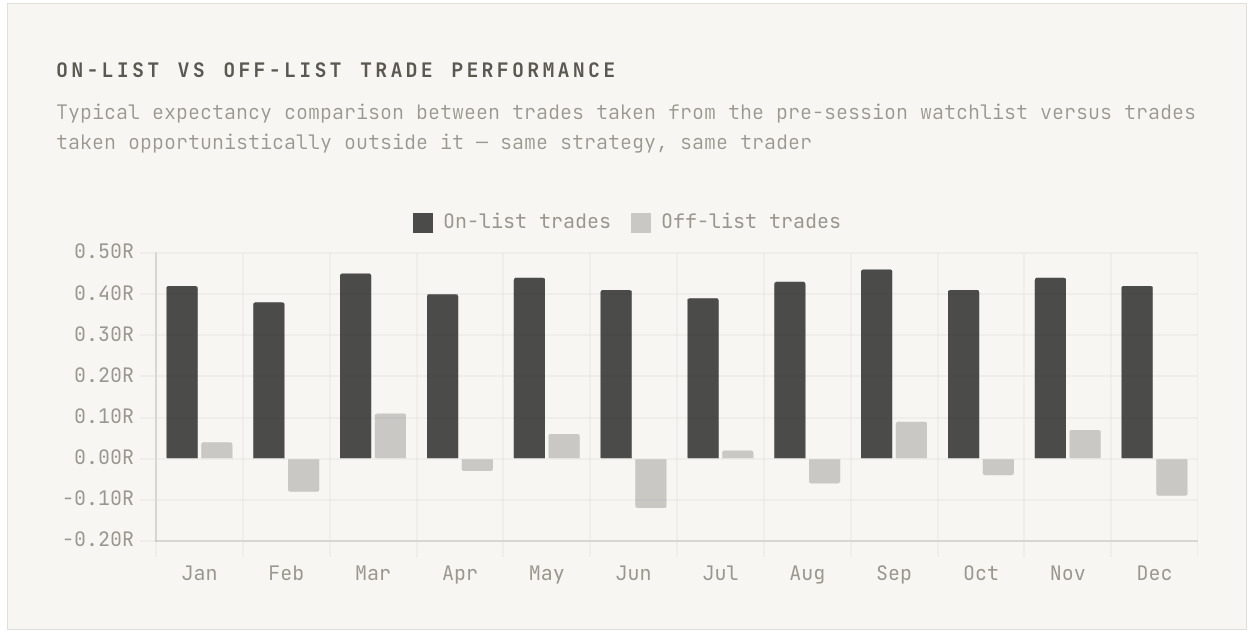

Trading outside the watchlist is not opportunism. It is the abandonment of the filtering process under real-time emotional pressure. The filtering process was designed to remove names that do not meet the strategy’s criteria. A name that was not on the watchlist because it failed the structural filter has not suddenly passed that filter because it is moving visibly during the session. The same criteria that excluded it this morning still apply. The trader who takes the trade anyway has not identified a new opportunity. They have overridden a filter with a real-time visual impression, which is precisely what the filter was designed to prevent.

The practical discipline is to treat the watchlist as a binding commitment for the session. Opportunities outside the list are logged for potential consideration in the next session’s filter process, not acted on in real time. If a name that was not on the watchlist appears genuinely compelling, the correct action is to note it, evaluate it against the full filter criteria after the session, and add it to the next session’s watchlist if it passes. This discipline feels restrictive during sessions when the off-list names are moving. It feels very different when the month-end review reveals that the off-list trades have consistently underperformed the on-list trades, which is almost always what the data shows.

PRACTICAL APPLICATION

Tag every trade in your journal as either on-list or off-list based on whether the name appeared on that session’s pre-session watchlist. Review this categorization monthly and calculate average R separately for each category. The gap between the two numbers is the direct cost of departing from the watchlist, expressed in R per trade. For most traders who have never tracked this distinction, the gap is large enough to be immediately motivating. For the minority whose off-list trades actually outperform on-list trades, the exercise reveals that the filtering process itself needs to be redesigned, which is equally valuable information.

CONCLUSION

The watchlist is one of the most undervalued components of a professional trading process. Most traders treat it as an afterthought — a rough collection of names assembled quickly before the session with no systematic filtering and no written scenarios. The results of that approach are embedded in the execution quality that follows: reactive decisions, inconsistent entry timing, trades taken in structurally unfavorable contexts, and a constant sense that opportunities are being missed because attention is spread too thin.

The watchlist built through the process described in this newsletter produces the opposite experience. The filtering stages remove the noise before the session begins. The scenario construction converts the remaining candidates into actionable plans rather than surveillance tasks. The regime assessment ensures the list reflects the actual character of the upcoming session rather than a generic template. The size constraint enforces quality over quantity. The pre-session review converts the plan from a document into executable knowledge. The session discipline keeps the trader within the prepared universe where the edge criteria are actually present.

None of this is intellectually complex. The complexity, such as it is, lies entirely in the consistency of application. A watchlist process that is followed rigorously for one week and then abandoned under the time pressure of a busy schedule produces no durable improvement. One that is built into the routine with the same non-negotiable status as the trading session itself produces compounding improvements in execution quality that become visible within a month and dramatic within a quarter.

A trader who arrives at the session with three names, three scenarios, and three invalidation levels is not less prepared than one who arrives with fifteen names and no plan. They are substantially more prepared. The session will confirm this within the first hour.